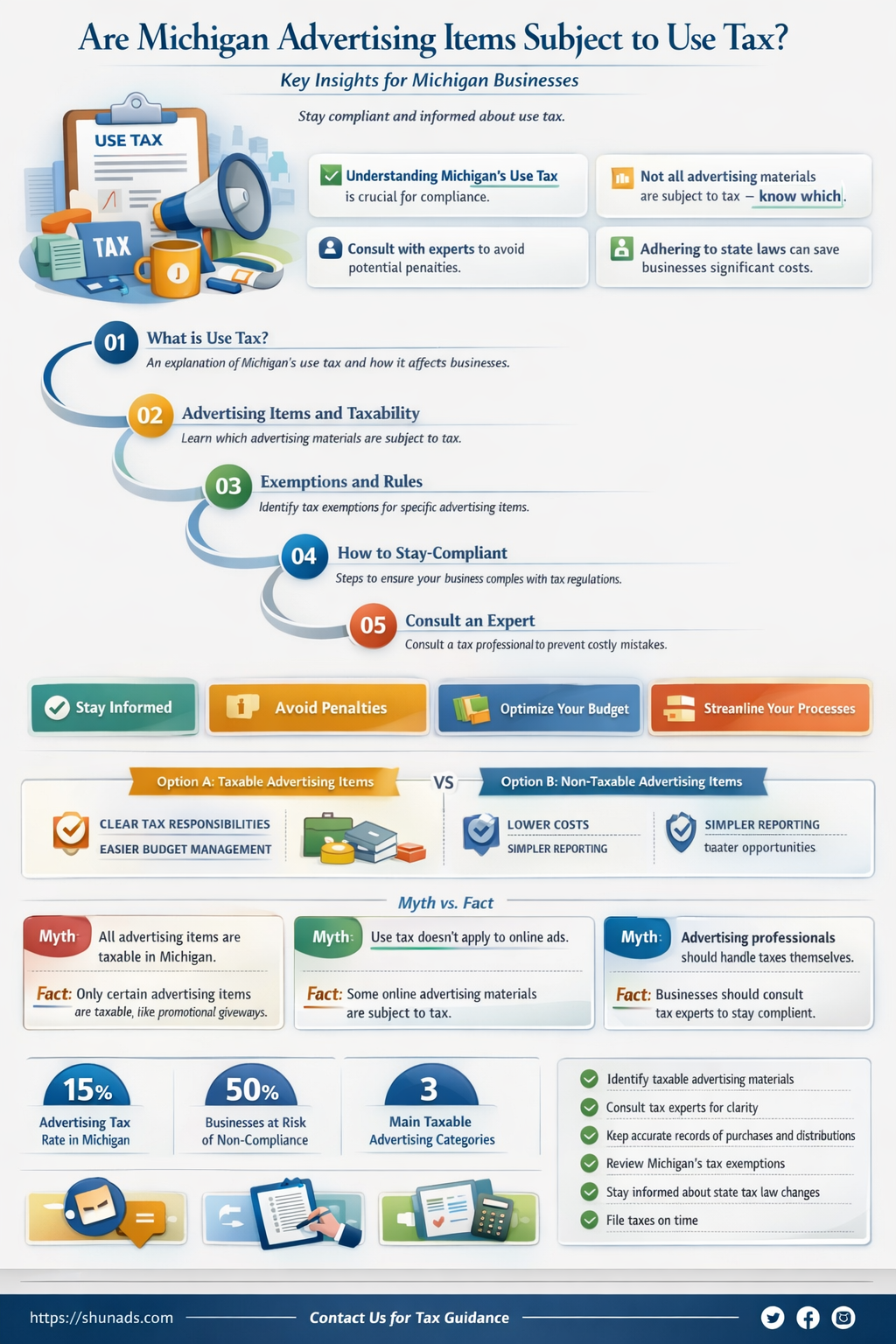

In Michigan, the question of whether advertising items are subject to use tax hinges on their classification and purpose. Use tax in Michigan applies to tangible personal property used, stored, or consumed in the state when sales tax has not been paid. Advertising items, such as promotional materials or branded merchandise, may be exempt from use tax if they are considered incidental advertising materials and meet specific criteria outlined by the Michigan Department of Treasury. These criteria often include the item’s value, distribution method, and whether it is given away for free as part of a marketing strategy. However, if the items are retained for business use or distributed in a way that does not qualify for the exemption, they may be subject to use tax. Understanding these distinctions is crucial for businesses to ensure compliance with Michigan’s tax regulations and avoid potential penalties.

| Characteristics | Values |

|---|---|

| Taxability of Advertising Items | In Michigan, tangible personal property used for advertising purposes may be subject to use tax if purchased without paying sales tax. |

| Exemptions | Certain promotional items given away for free may be exempt if they meet specific criteria (e.g., low cost, imprinted with the business name). |

| Use Tax Applicability | Use tax applies if the items are purchased out-of-state or from an unregistered vendor and used in Michigan. |

| Threshold for Taxability | Items valued above a certain threshold (e.g., not de minimis) are generally taxable. |

| Reporting Requirements | Businesses must report and remit use tax on taxable advertising items through their Michigan sales and use tax returns. |

| Examples of Taxable Items | Promotional pens, mugs, t-shirts, and other tangible items used for advertising purposes. |

| Non-Taxable Items | Digital advertising materials (e.g., online ads) and services are not subject to use tax. |

| Recent Updates | As of the latest data (2023), Michigan has not introduced specific exemptions for advertising items beyond general use tax rules. |

| Enforcement | The Michigan Department of Treasury enforces use tax compliance, including audits of businesses using advertising items. |

Explore related products

![Communication from Board of State Tax Commissioners to House of Representatives Transmitting Data Relative to Operation of Tax Laws. February 22, 1911. Ordered Printed for Use 1911 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

What You'll Learn

![]()

Taxable Items Definition

In Michigan, the definition of taxable items is crucial for determining whether advertising materials are subject to use tax. The state’s tax code categorizes tangible personal property as taxable, but exceptions and nuances exist, particularly for items used in business operations. Advertising items, such as promotional pens, brochures, or branded merchandise, often straddle the line between taxable and exempt, depending on their intended use and distribution. For instance, if these items are given away for free to promote a business, they may not be considered a retail sale and thus could escape taxation. However, if they are sold or if their cost is included in a taxable transaction, they fall under the taxable umbrella. Understanding this distinction is essential for businesses to comply with Michigan’s use tax regulations and avoid penalties.

Analyzing the taxable items definition further, it’s important to note that Michigan’s use tax applies to items purchased out-of-state for use in Michigan, where sales tax was not collected at the point of purchase. This includes advertising materials bought from vendors in other states. For example, if a Michigan business orders custom promotional mugs from an Ohio supplier and no sales tax is charged, the business is responsible for remitting use tax to Michigan. The key factor here is the item’s ultimate use—if the mugs are distributed for free as part of a marketing campaign, they may not be taxable, but if they are sold or their cost is bundled into a taxable service, they become subject to tax. Businesses must carefully track these transactions to ensure accurate tax reporting.

From a practical standpoint, businesses should implement clear guidelines for classifying advertising items. Start by documenting the purpose of each item—is it for free distribution, resale, or internal use? For instance, branded t-shirts given to employees are exempt from tax, while those sold at a company event are taxable. Additionally, maintain detailed records of purchases, including invoices and receipts, to substantiate tax positions during audits. A proactive approach involves consulting Michigan’s Department of Treasury guidelines or a tax professional to clarify ambiguous cases, such as whether digital advertising materials (e.g., downloadable content) qualify as tangible personal property.

Comparatively, Michigan’s approach to taxing advertising items aligns with broader trends in state tax law but differs in specific interpretations. While some states exempt all promotional giveaways, Michigan focuses on the transaction context. For example, California exempts promotional items if their cost per item is under $2, whereas Michigan’s rules are more transactional. This highlights the need for businesses operating across states to tailor their tax strategies to each jurisdiction. In Michigan, the takeaway is clear: the taxable status of advertising items hinges on their role in a transaction, not just their nature as promotional tools.

Finally, a persuasive argument for compliance is the potential financial impact of misclassifying advertising items. Penalties for unpaid use tax in Michigan can include interest, fines, and even legal action. For small businesses, these costs can be crippling. By investing time upfront to understand the taxable items definition and applying it rigorously, companies can avoid costly mistakes. Regularly reviewing tax policies and training staff on proper classification ensures long-term compliance. In the end, treating advertising items with the same scrutiny as other business purchases is not just a legal obligation—it’s a strategic safeguard for financial health.

Colleges Should Avoid Social Media Advertising: Privacy, Distraction, and Inequality Concerns

You may want to see also

Explore related products

![]()

Exemptions for Resale

In Michigan, advertising items purchased for resale are generally exempt from use tax, provided specific conditions are met. This exemption hinges on the intent to resell the items in their original form, without alteration or incorporation into a larger product. For instance, if a business buys promotional pens to sell directly to customers, these items qualify for the resale exemption. However, if the pens are customized with a company logo before distribution, they may no longer qualify, as customization can alter their resale nature.

To claim this exemption, businesses must maintain detailed records, including resale certificates from purchasers. These certificates serve as proof that the items were sold to a buyer who intends to resell them. For example, a distributor purchasing branded tote bags for resale to retailers would provide a resale certificate to the original seller, ensuring the transaction remains tax-exempt. Failure to obtain or retain these certificates can result in the business being liable for use tax on the purchase.

A critical distinction exists between items resold as-is and those used for promotional purposes. If advertising items are given away for free or used internally, they do not qualify for the resale exemption. For instance, a company distributing branded mugs as gifts to clients would owe use tax on the purchase, as the mugs are not being resold. This highlights the importance of clearly separating inventory intended for resale from that used for promotional activities.

Practical tips for navigating this exemption include segregating resale inventory from promotional stock and training staff to recognize the difference. Businesses should also regularly audit their records to ensure compliance, as Michigan’s Department of Treasury scrutinizes resale claims closely. By adhering to these guidelines, companies can avoid unexpected tax liabilities while leveraging the resale exemption to reduce costs on advertising items.

Who Handles Goodwill's Advertising Campaigns? Unveiling Their Marketing Strategy

You may want to see also

Explore related products

![]()

Use Tax Calculation

In Michigan, determining whether advertising items are subject to use tax hinges on their intended use and the nature of the transaction. Use tax is essentially a companion to sales tax, levied on tangible personal property purchased outside the state but used, stored, or consumed within Michigan. When calculating use tax for advertising items, the first step is to ascertain if the items are considered tangible personal property. Promotional materials like pens, calendars, or branded merchandise typically fall into this category, making them potentially taxable.

The calculation of use tax begins with identifying the total purchase price of the advertising items, including shipping and handling charges. Michigan’s use tax rate mirrors its sales tax rate, currently set at 6%. For instance, if a business purchases $1,000 worth of promotional mugs from an out-of-state vendor, the use tax due would be $60 ($1,000 × 0.06). It’s crucial to exclude any items that are exempt from taxation, such as those used exclusively for resale or certain manufacturing processes, though advertising items rarely qualify for these exemptions.

One common pitfall in use tax calculation is overlooking the cumulative effect of multiple small purchases. Michigan requires businesses to remit use tax if their total out-of-state purchases exceed $100 in a calendar year. For example, a company buying $50 worth of branded keychains in January and $70 worth of custom notebooks in March would owe use tax on the combined $120 expenditure. Tracking these transactions meticulously is essential to avoid penalties for underpayment.

Another critical aspect is understanding when use tax applies versus sales tax. If the out-of-state vendor collects Michigan sales tax at the point of purchase, no additional use tax is due. However, if the vendor does not collect sales tax, the responsibility falls on the purchaser to self-assess and remit use tax. This distinction often catches businesses off guard, particularly those accustomed to vendors handling tax collection.

In conclusion, calculating use tax for advertising items in Michigan requires a clear understanding of the items’ classification, the total purchase price, and the state’s tax thresholds. By staying vigilant about tracking purchases and understanding the interplay between sales and use tax, businesses can ensure compliance and avoid unnecessary financial liabilities. Practical tips include maintaining detailed records of out-of-state purchases and consulting Michigan’s Department of Treasury guidelines for specific scenarios.

Exploring Social Media Ads: Types, Strategies, and Platforms Dominating Today

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![]()

Reporting Requirements

In Michigan, businesses must report use tax on advertising items when they are purchased without tax from out-of-state vendors and used within the state. This requirement hinges on the items’ tangible nature and their distribution to the public, such as branded pens, calendars, or tote bags. Reporting must occur on the Michigan Sales and Use Tax Return (Form 5080), with the tax calculated at the current rate of 6%. Failure to comply can result in penalties, including interest on unpaid amounts and fines up to 25% of the tax due.

To ensure accurate reporting, businesses should maintain detailed records of all advertising item purchases, including invoices, receipts, and documentation of their intended use. For instance, if a company buys 500 custom notebooks for $1,500 from an out-of-state supplier, the use tax calculation would be $90 ($1,500 × 6%). This amount must be reported on Line 1 of Form 5080, with the total tax due included on Line 19. Quarterly filing is mandatory for most businesses, though annual filing may be permitted for those with minimal tax liability.

A common pitfall is misclassifying advertising items as exempt from use tax. For example, items given to employees for personal use (e.g., a company-branded jacket) are not subject to use tax, but those distributed to clients or the public are taxable. Businesses should also be cautious when purchasing items in bulk; even if the vendor does not collect sales tax, the use tax obligation still applies. Cross-referencing Michigan’s Department of Treasury guidelines can clarify ambiguous cases, such as whether digital advertising materials (e.g., USB drives preloaded with promotional content) qualify as tangible personal property.

For businesses operating across multiple states, Michigan’s use tax reporting can be particularly complex. If a company has nexus in Michigan—whether through physical presence, economic activity, or affiliate relationships—it must register for a sales tax license and report use tax accordingly. E-commerce businesses, for instance, should track Michigan-based customers receiving advertising items and ensure compliance with the state’s reporting thresholds. Utilizing tax software or consulting a tax professional can streamline this process and mitigate risks.

Ultimately, proactive management of reporting requirements is essential to avoid audits and penalties. Businesses should conduct periodic self-reviews, verifying that all advertising item purchases are accounted for and that use tax is calculated and remitted correctly. Michigan’s Voluntary Disclosure Program offers a pathway for businesses to rectify past non-compliance with reduced penalties, provided they self-report before being contacted by the state. By staying informed and organized, businesses can navigate Michigan’s use tax landscape with confidence.

Competitor Name Psychology: Why Advertisers Avoid Direct Brand Mentions

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UY218_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UY218_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UY218_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UY218_.jpg)

![]()

Penalties for Non-Compliance

Non-compliance with Michigan’s use tax laws, particularly regarding advertising items, can trigger a cascade of penalties that escalate quickly. The Michigan Department of Treasury imposes a late payment penalty of 5% of the unpaid tax for each month (or fraction thereof) the tax remains unpaid, capped at 25%. Additionally, interest accrues at a variable rate, currently set at 5% annually, compounding daily. These financial penalties are not merely punitive; they reflect the state’s effort to deter businesses from neglecting their tax obligations, especially when promotional materials cross state lines and fall under use tax jurisdiction.

Beyond monetary penalties, non-compliance risks audits and legal action. Michigan’s tax authorities may conduct a thorough examination of a business’s records, often extending beyond the initial scope of the violation. For instance, a business found non-compliant with use tax on promotional items might face scrutiny of its entire sales and use tax history. Repeat offenders or those deemed willfully negligent could face criminal charges, including fines up to $10,000 and potential imprisonment. Such outcomes underscore the importance of proactive compliance, particularly for businesses operating in multiple states with varying tax regulations.

A lesser-known consequence of non-compliance is the damage to a business’s reputation and operational stability. Vendors and clients may hesitate to engage with a company flagged for tax violations, fearing indirect liability or instability. For small businesses, this reputational hit can be devastating, often outweighing the immediate financial penalties. Moreover, non-compliant businesses may be barred from participating in state contracts or programs, further limiting growth opportunities. This collateral damage highlights why understanding and adhering to use tax laws is not just a legal obligation but a strategic business imperative.

To mitigate these risks, businesses should implement robust internal controls and seek professional guidance. Regularly reviewing procurement records for advertising items, such as branded merchandise sourced from out-of-state vendors, can identify potential use tax liabilities. Utilizing tax software or consulting a tax specialist can ensure accurate calculations and timely filings. For businesses operating on tight margins, the cost of compliance pales in comparison to the penalties and long-term consequences of non-compliance. In Michigan’s stringent tax environment, prevention is not just cheaper—it’s essential.

Maximize ROI with Microsoft Advertising Intelligence: Strategies for Success

You may want to see also

Frequently asked questions

Yes, advertising items purchased for use in Michigan are generally subject to use tax if sales tax was not paid at the time of purchase.

Advertising items include promotional materials like pens, keychains, brochures, or any other items used to promote a business, even if given away for free.

Yes, if you purchased advertising items out of state and did not pay sales tax, you are required to pay Michigan use tax when using them in Michigan.

There are no specific exemptions for advertising items. However, if the items are resold or used in a way that qualifies for another exemption, use tax may not apply.

Use tax on advertising items should be reported and paid on your Michigan sales and use tax return (Form 5080) or through the Michigan Treasury Online system.

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UY218_.jpg)

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UY218_.jpg)