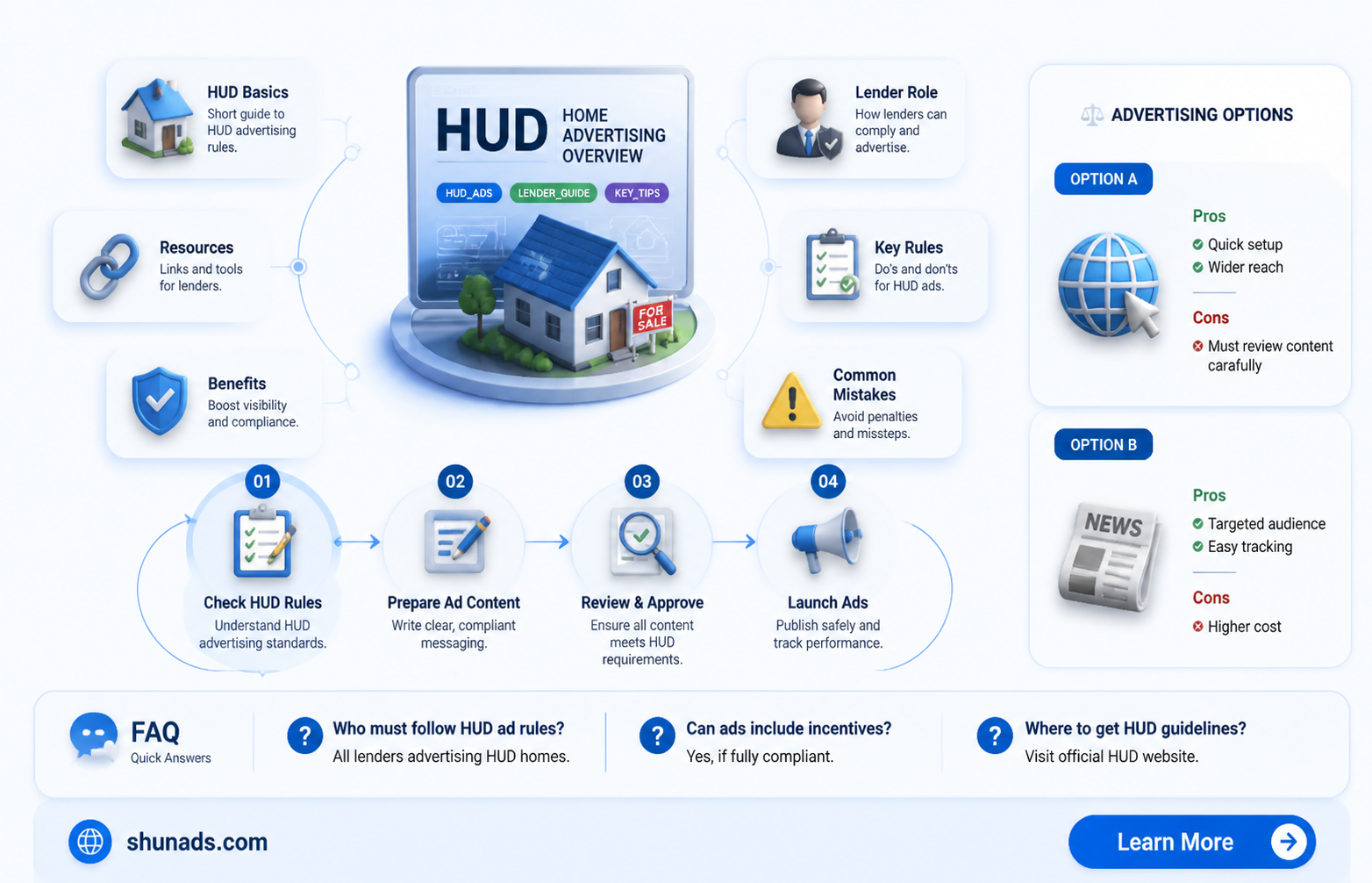

The topic of whether a lender can advertise HUD homes is an important one in the realm of real estate and mortgage lending. HUD homes, which are properties owned by the U.S. Department of Housing and Urban Development, often present unique opportunities for both buyers and lenders. However, there are specific guidelines and regulations that must be followed when it comes to advertising these properties. In this paragraph, we will explore the intricacies of advertising HUD homes, including the roles and responsibilities of lenders, the importance of compliance with HUD guidelines, and the potential benefits for both lenders and borrowers in the HUD home market.

Explore related products

What You'll Learn

- HUD Home Eligibility: Requirements for lenders to advertise HUD homes, including FHA approval and compliance with HUD regulations

- Advertising Guidelines: HUD's rules on how lenders can market HUD homes, ensuring transparency and avoiding misleading information

- Lender Responsibilities: Duties of lenders when advertising HUD homes, such as providing accurate property information and ensuring equal opportunity

- Benefits of HUD Homes: Advantages for lenders in advertising HUD homes, including potential for increased business and community development

- Common Pitfalls: Mistakes lenders should avoid when advertising HUD homes, like misrepresenting property conditions or violating fair housing laws

![]()

HUD Home Eligibility: Requirements for lenders to advertise HUD homes, including FHA approval and compliance with HUD regulations

To advertise HUD homes, lenders must meet specific eligibility requirements set forth by the Department of Housing and Urban Development. One of the primary prerequisites is obtaining FHA approval, which ensures that the lender is authorized to participate in FHA-insured mortgage programs. This approval process involves a thorough evaluation of the lender's financial stability, operational integrity, and compliance with FHA guidelines.

In addition to FHA approval, lenders must also comply with HUD regulations governing the advertising of HUD homes. These regulations are designed to ensure that all marketing materials are accurate, transparent, and free from discrimination. Lenders are required to include specific disclosures in their advertisements, such as the FHA logo and a statement indicating that the property is HUD-owned. Furthermore, they must adhere to HUD's guidelines on pricing, which dictate that the advertised price should reflect the property's fair market value.

Lenders should also be aware of the different types of HUD homes available for advertising. These include properties that are currently occupied, vacant, or in need of repair. Each type of property may have unique advertising requirements and restrictions, so lenders must familiarize themselves with HUD's guidelines for each category. For example, lenders may need to disclose the condition of the property or provide additional information about the repair process.

To maintain their eligibility to advertise HUD homes, lenders must undergo regular reviews and audits by HUD. These reviews ensure that lenders are continuing to meet all applicable regulations and guidelines. Lenders should also stay up-to-date on any changes to HUD's policies and procedures, as failure to comply with these updates can result in the loss of their advertising privileges.

In summary, lenders must navigate a complex set of requirements to advertise HUD homes, including obtaining FHA approval, complying with HUD regulations, and staying informed about policy changes. By meeting these eligibility criteria, lenders can gain access to a valuable market segment and help facilitate the sale of HUD-owned properties.

Can Rhode Island Judges Advertise? Legal Ethics and Rules Explained

You may want to see also

Explore related products

![]()

Advertising Guidelines: HUD's rules on how lenders can market HUD homes, ensuring transparency and avoiding misleading information

The U.S. Department of Housing and Urban Development (HUD) has established specific guidelines for lenders to advertise HUD homes, ensuring that the marketing is transparent and free from misleading information. These guidelines are crucial for maintaining the integrity of the HUD home sales process and protecting potential buyers from deceptive practices.

One key aspect of HUD's advertising guidelines is the requirement for lenders to clearly disclose that the property is a HUD home. This disclosure must be prominently featured in all advertisements, including online listings, print ads, and signage. Additionally, lenders must provide accurate information about the property's condition, price, and any special financing options available through HUD.

HUD also prohibits lenders from making false or misleading statements about the property's value or condition. This includes exaggerating the property's features, downplaying its flaws, or making unsubstantiated claims about its potential for appreciation. Lenders must also refrain from using high-pressure sales tactics or making promises that cannot be fulfilled.

To ensure compliance with these guidelines, HUD recommends that lenders develop a comprehensive advertising policy that outlines the specific rules and procedures for marketing HUD homes. This policy should be communicated to all employees involved in the advertising process and regularly reviewed to ensure that it remains up-to-date and effective.

In conclusion, HUD's advertising guidelines play a vital role in ensuring that lenders market HUD homes in a transparent and ethical manner. By following these guidelines, lenders can help potential buyers make informed decisions and avoid the pitfalls of deceptive advertising practices.

Measuring Ad Campaign Success: Key Metrics and Strategies for Optimal Results

You may want to see also

Explore related products

![]()

Lender Responsibilities: Duties of lenders when advertising HUD homes, such as providing accurate property information and ensuring equal opportunity

Lenders have a critical role to play when advertising HUD homes, and their responsibilities are multifaceted. One of the primary duties is to provide accurate property information to potential buyers. This includes details about the property's condition, location, and any known defects or issues. Lenders must also ensure that the advertising materials are free from any misleading or false statements that could mislead potential buyers.

In addition to providing accurate information, lenders must also ensure equal opportunity for all potential buyers. This means that they cannot discriminate against any individual or group based on factors such as race, color, religion, sex, or national origin. Lenders must also make sure that their advertising materials are accessible to individuals with disabilities, and that they comply with all applicable fair housing laws and regulations.

Another important responsibility of lenders is to ensure that their advertising materials are transparent and clear. This includes providing information about the financing options available, the interest rates, and any fees or costs associated with the purchase. Lenders must also make sure that their advertising materials do not create unrealistic expectations or make false promises to potential buyers.

Furthermore, lenders must also be aware of the specific requirements and guidelines set forth by HUD for advertising their homes. This includes following the HUD Advertising Guidelines, which outline the acceptable practices for advertising HUD homes. Lenders must also ensure that their advertising materials comply with all applicable state and local laws and regulations.

In conclusion, lenders play a crucial role in the advertising of HUD homes, and their responsibilities are significant. By providing accurate property information, ensuring equal opportunity, and complying with all applicable laws and regulations, lenders can help to ensure that the advertising of HUD homes is fair, transparent, and effective.

Get Paid to Advertise for Goodyear: Opportunities and How to Apply

You may want to see also

Explore related products

![]()

Benefits of HUD Homes: Advantages for lenders in advertising HUD homes, including potential for increased business and community development

Lenders who advertise HUD homes can significantly increase their business opportunities. By promoting these properties, lenders can attract a wider range of potential borrowers, including those who may not have considered purchasing a home otherwise. This can lead to an increase in loan applications and, ultimately, more closed loans. Additionally, lenders who specialize in HUD homes may develop a reputation as experts in this area, which can further enhance their business prospects.

Advertising HUD homes can also contribute to community development. These properties are often located in areas that are in need of revitalization, and by promoting them, lenders can help to attract new residents and businesses to these neighborhoods. This can lead to increased economic activity, improved property values, and a stronger sense of community. Furthermore, HUD homes are often more affordable than other properties, which can make homeownership more accessible to low- and moderate-income individuals and families.

Another advantage for lenders is that HUD homes are backed by the federal government, which can reduce the risk associated with lending on these properties. This can make it easier for lenders to offer more favorable loan terms, such as lower interest rates or longer repayment periods, which can be more attractive to borrowers. Additionally, the government backing can provide lenders with greater confidence in the value of the property, which can reduce the likelihood of loan defaults.

Lenders who advertise HUD homes can also benefit from the increased visibility that comes with promoting these properties. By highlighting their expertise in this area, lenders can attract more attention from potential borrowers, real estate agents, and other industry professionals. This can lead to more referrals and, ultimately, more business opportunities. Furthermore, lenders who are proactive in advertising HUD homes may be seen as more innovative and forward-thinking, which can help them to stand out in a competitive market.

In conclusion, lenders who advertise HUD homes can benefit from increased business opportunities, contributions to community development, reduced lending risks, and enhanced visibility in the marketplace. By promoting these properties, lenders can attract a wider range of potential borrowers, develop a reputation as experts in this area, and contribute to the revitalization of neighborhoods in need.

Unlock Free Phones: How One Cellphone Can Fund Another Through Ads

You may want to see also

Explore related products

![]()

Common Pitfalls: Mistakes lenders should avoid when advertising HUD homes, like misrepresenting property conditions or violating fair housing laws

Lenders advertising HUD homes must navigate a complex landscape of regulations and ethical considerations to avoid common pitfalls that can lead to legal repercussions and damage to their reputation. One significant mistake is misrepresenting property conditions, which can occur through misleading advertisements or failing to disclose known defects. This not only violates HUD guidelines but also sets unrealistic expectations for potential buyers, leading to dissatisfaction and potential legal disputes.

Another critical error is violating fair housing laws, which prohibit discrimination based on race, color, religion, sex, national origin, disability, or familial status. Lenders must ensure that their advertising materials do not inadvertently or overtly discriminate against any protected groups. For instance, using language that suggests a preference for certain types of buyers or displaying images that imply exclusivity can be problematic.

To avoid these pitfalls, lenders should implement a thorough review process for all advertising materials, ensuring that they accurately reflect the property's condition and comply with fair housing regulations. This includes conducting regular training sessions for staff involved in the advertising process to keep them informed about the latest guidelines and best practices. Additionally, lenders should engage with diverse communities and seek feedback from a variety of stakeholders to ensure that their advertising efforts are inclusive and respectful.

In conclusion, by being vigilant about property condition representations and adhering to fair housing laws, lenders can avoid common advertising pitfalls and foster a more equitable and transparent housing market. This not only benefits potential buyers but also helps lenders maintain their integrity and avoid costly legal issues.

EU TV Ad Ban: Why Pharma Stays Silent on European Screens

You may want to see also

Frequently asked questions

Yes, a lender can advertise HUD homes, but they must follow specific guidelines set by the Department of Housing and Urban Development (HUD).

Lenders must ensure that their advertisements are accurate, do not discriminate against any protected classes, and comply with HUD's advertising regulations. They must also clearly state that the property is HUD-owned and that the sale is subject to HUD's approval.

No, lenders cannot advertise HUD homes before they are officially listed by HUD. This is to ensure that all potential buyers have an equal opportunity to view and bid on the properties.

Yes, there are restrictions on who can buy HUD homes. For example, HUD homes are typically reserved for owner-occupants and cannot be purchased by investors for resale. Additionally, buyers must meet certain income and credit requirements to qualify for a HUD home.