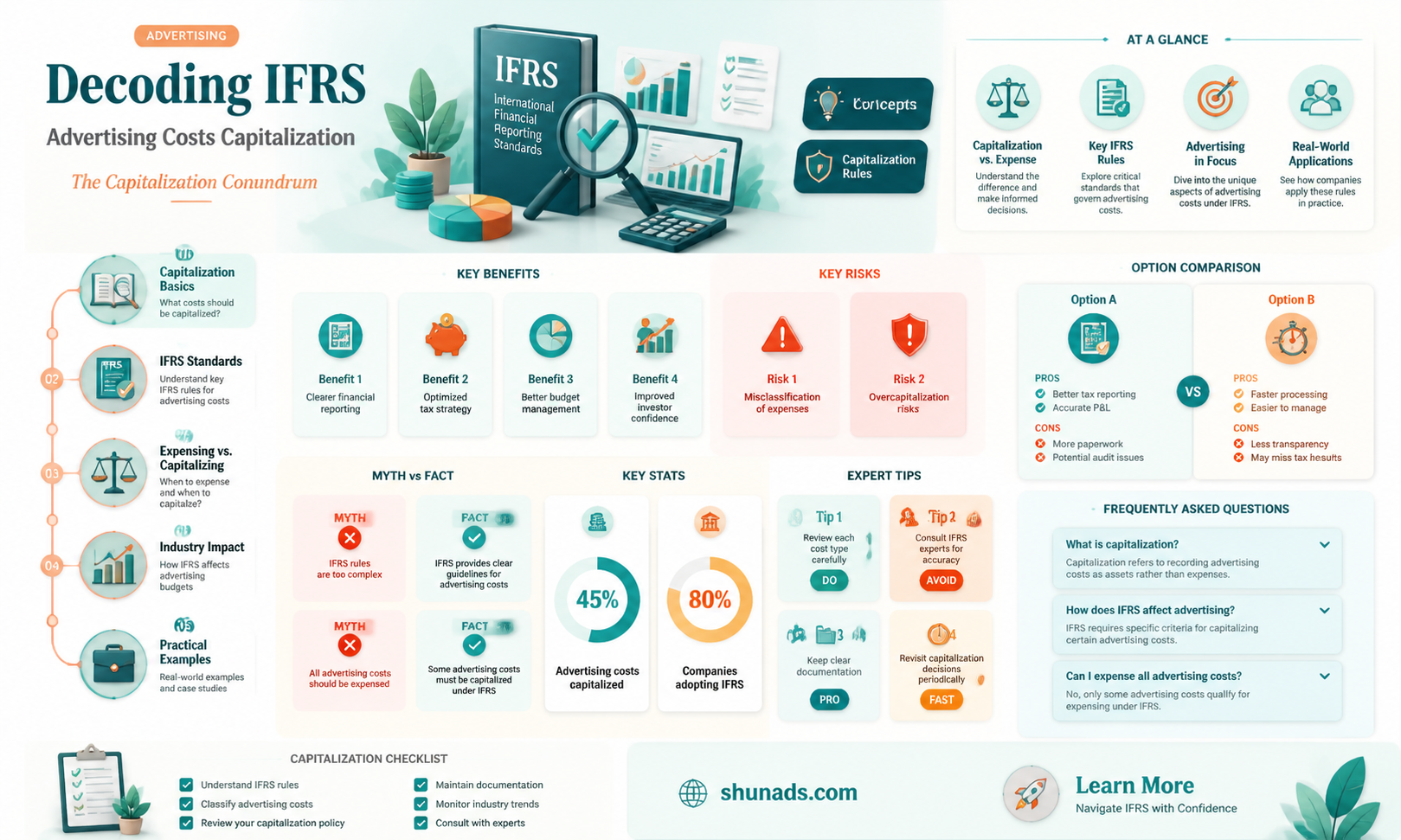

Advertising costs under IFRS (International Financial Reporting Standards) are typically treated as expenses when incurred, meaning they are recorded on the income statement and reduce net income for the period in which they are spent. However, there are specific circumstances where advertising costs can be capitalized. For instance, if the advertising campaign is part of a broader marketing initiative that spans multiple reporting periods, the costs may be capitalized and amortized over the useful life of the campaign. This treatment is consistent with the IFRS principle of matching costs with revenues, ensuring that expenses are recognized in the same period as the revenues they help generate. Companies must carefully evaluate their advertising strategies and the expected benefits to determine whether capitalization is appropriate.

Explore related products

What You'll Learn

- IFRS 15 Overview: Understand the framework governing revenue recognition and its implications for advertising costs

- Capitalization Criteria: Explore the specific conditions under which advertising costs can be capitalized according to IFRS

- Amortization Methods: Learn about the different approaches to amortizing capitalized advertising costs over their useful life

- Disclosure Requirements: Discover the necessary disclosures for capitalized advertising costs in financial statements under IFRS

- Practical Examples: Analyze real-world scenarios illustrating the application of IFRS rules to advertising cost capitalization

![]()

IFRS 15 Overview: Understand the framework governing revenue recognition and its implications for advertising costs

IFRS 15, titled "Revenue from Contracts with Customers," is a comprehensive standard that governs how companies recognize revenue from their customer contracts. It was issued by the International Accounting Standards Board (IASB) and is designed to provide a consistent framework for revenue recognition across different industries and jurisdictions. This standard has significant implications for advertising costs, as it outlines specific criteria for when these costs can be capitalized and amortized over time.

Under IFRS 15, advertising costs are generally considered to be incremental costs incurred to obtain a contract with a customer. These costs can include expenditures on marketing campaigns, promotional materials, and other advertising activities that are directly related to acquiring new customers or retaining existing ones. To be eligible for capitalization, these costs must meet certain criteria, such as being identifiable, measurable, and directly attributable to the acquisition of a specific customer contract.

Once capitalized, advertising costs are typically amortized over the expected life of the customer contract. This means that the costs are spread out over time, rather than being expensed immediately. The amortization period is determined based on the expected duration of the customer relationship and the pattern of revenue recognition. For example, if a company expects to generate revenue from a customer contract over a period of five years, the advertising costs associated with that contract would be amortized over the same five-year period.

It's important to note that IFRS 15 does not allow for the capitalization of all advertising costs. Costs that are not directly related to obtaining a specific customer contract, such as general brand awareness campaigns or promotional activities that are not tied to a particular contract, must be expensed as incurred. Additionally, companies must carefully consider the recoverability of their advertising costs, as these costs can only be capitalized if they are expected to be recovered through future revenue generation.

In conclusion, IFRS 15 provides a clear framework for the capitalization and amortization of advertising costs. By understanding the specific criteria outlined in this standard, companies can ensure that they are accurately recognizing revenue and expenses related to their advertising activities. This can help to improve financial reporting and provide a more accurate picture of a company's financial performance.

Advertising on Angie's List: Opportunities, Benefits, and How to Get Started

You may want to see also

Explore related products

![]()

Capitalization Criteria: Explore the specific conditions under which advertising costs can be capitalized according to IFRS

According to IFRS, advertising costs can be capitalized under specific conditions. One such condition is that the costs must be directly attributable to the acquisition of a new customer or the retention of an existing customer. This means that the advertising campaign must be specifically targeted at acquiring new customers or retaining existing ones, and the costs must be able to be directly linked to this objective.

Another condition for capitalizing advertising costs is that the costs must be significant. This means that the costs must be material in relation to the company's overall financial position and performance. In other words, the costs must be substantial enough to have a significant impact on the company's financial statements.

Additionally, the advertising costs must be incurred during a specific period. This period is typically defined as the period during which the advertising campaign is running. The costs must be incurred during this period in order to be capitalized.

It is also important to note that the advertising costs must be recoverable. This means that the company must be able to recover the costs through future revenue streams. In other words, the advertising campaign must be expected to generate sufficient revenue to cover the costs incurred.

Finally, the company must have a clear and consistent policy for capitalizing advertising costs. This policy must be applied consistently across all advertising campaigns and must be clearly communicated to all stakeholders.

In summary, advertising costs can be capitalized under IFRS if they are directly attributable to the acquisition or retention of customers, are significant, are incurred during a specific period, are recoverable, and are subject to a clear and consistent policy.

Advertising's Dual Edge: Informing Truths and Spreading Misinformation

You may want to see also

Explore related products

![]()

Amortization Methods: Learn about the different approaches to amortizing capitalized advertising costs over their useful life

Under International Financial Reporting Standards (IFRS), companies have the flexibility to choose from several amortization methods for their capitalized advertising costs. These methods include the straight-line method, the declining balance method, and the units-of-production method. Each method has its own advantages and disadvantages, and the choice of method can significantly impact a company's financial statements.

The straight-line method is the most common amortization method used for capitalized advertising costs. Under this method, the cost of the advertising campaign is evenly distributed over its useful life. For example, if a company spends $100,000 on an advertising campaign that is expected to last for five years, the annual amortization expense would be $20,000. This method is simple to implement and understand, but it may not accurately reflect the actual consumption of the advertising campaign's benefits.

The declining balance method is another popular amortization method. This method involves applying a fixed percentage to the remaining balance of the advertising campaign's cost at the beginning of each period. The percentage used is typically higher than the straight-line method, which results in a higher amortization expense in the early years of the campaign's life. This method can be more accurate in reflecting the actual consumption of the campaign's benefits, as it assumes that the benefits of the campaign are consumed more quickly in the early years.

The units-of-production method is a more complex amortization method that involves allocating the cost of the advertising campaign based on the number of units produced or sold. This method can be more accurate in reflecting the actual consumption of the campaign's benefits, as it directly ties the amortization expense to the production or sales activity. However, this method can be more difficult to implement and requires more detailed tracking of production or sales data.

Companies should carefully consider the different amortization methods available under IFRS and choose the method that best reflects the actual consumption of the advertising campaign's benefits. The choice of method can have a significant impact on a company's financial statements and should be made in consultation with a qualified accountant.

Decoding Real Estate Jargon: The Use of Abbreviations in Property Listings

You may want to see also

Explore related products

![]()

Disclosure Requirements: Discover the necessary disclosures for capitalized advertising costs in financial statements under IFRS

Under IFRS, companies are required to make specific disclosures regarding capitalized advertising costs in their financial statements. These disclosures are crucial for providing transparency and ensuring that stakeholders have a clear understanding of the company's financial position and performance. The necessary disclosures include the amount of advertising costs capitalized, the method used to amortize these costs, and the estimated useful life of the advertising assets.

Companies must also disclose the gross amount of advertising costs incurred, as well as the amount of advertising costs expensed in the period. This information allows stakeholders to assess the company's advertising strategy and evaluate the effectiveness of its advertising expenditures. Additionally, companies are required to disclose any impairment losses recognized on advertising assets, providing insight into the potential risks and uncertainties associated with these assets.

The disclosures related to capitalized advertising costs under IFRS are designed to enhance the comparability and reliability of financial statements. By providing detailed information about advertising costs, companies can help stakeholders make informed decisions and better understand the company's financial health. It is essential for companies to carefully consider these disclosure requirements and ensure that they are fully compliant with IFRS standards.

In practice, companies may face challenges in determining the appropriate method for amortizing advertising costs and estimating their useful life. IFRS allows for different amortization methods, such as straight-line, declining balance, or units of production, and companies must choose the method that best reflects the expected pattern of benefit from the advertising assets. This decision can have a significant impact on the company's financial statements and should be carefully considered.

Overall, the disclosure requirements for capitalized advertising costs under IFRS play a vital role in promoting transparency and accountability in financial reporting. By providing comprehensive information about advertising costs, companies can help stakeholders gain a deeper understanding of their financial performance and make more informed decisions.

Car-Wrap Advertising: A Realistic Way to Earn Extra Income?

You may want to see also

Explore related products

![]()

Practical Examples: Analyze real-world scenarios illustrating the application of IFRS rules to advertising cost capitalization

In the realm of International Financial Reporting Standards (IFRS), the capitalization of advertising costs is a nuanced topic. To illustrate this, let's delve into a real-world scenario involving a multinational consumer goods company, XYZ Inc. This company launched a significant advertising campaign for a new product line in 2022. The campaign spanned multiple media platforms, including television, social media, and print, incurring substantial costs.

Under IFRS, advertising costs are generally expensed as incurred. However, XYZ Inc. decided to capitalize a portion of these costs, arguing that they were directly related to the development of a new brand, which qualified as an intangible asset. This decision was based on IFRS 3, which allows for the capitalization of costs that are directly attributable to the acquisition or creation of an intangible asset.

The company's financial statements for 2022 reflected this capitalization, with a significant portion of the advertising expenditure being recorded as an asset on the balance sheet. This approach had a positive impact on the company's reported profits for the year, as it reduced the immediate expense recognized in the income statement.

However, this treatment is not without controversy. Some stakeholders argued that XYZ Inc. was aggressively interpreting the IFRS rules to enhance its financial performance. They pointed out that the costs capitalized were not directly related to the creation of an intangible asset but were rather general advertising expenses.

This scenario highlights the complexities and potential for differing interpretations when applying IFRS rules to advertising cost capitalization. It underscores the importance of careful analysis and consideration of the specific circumstances surrounding each advertising campaign to ensure compliance with IFRS standards.

In conclusion, while IFRS generally requires advertising costs to be expensed, there are instances where capitalization may be appropriate, particularly when costs are directly related to the development of a new brand or intangible asset. Companies must navigate these rules with caution, ensuring that their treatment of advertising costs aligns with the principles and requirements of IFRS.

Advertising Breast Augmentation on Facebook: Policies, Challenges, and Best Practices

You may want to see also

Frequently asked questions

Generally, advertising costs are expensed as incurred under IFRS because they are considered operational expenses that do not meet the criteria for capitalization as assets.

Costs can be capitalized under IFRS if they meet the criteria of being probable future economic benefits controlled by the entity, attributable to an identifiable asset, and measurable with sufficient reliability.

There are no specific exceptions under IFRS for capitalizing advertising costs. They are typically expensed as they are incurred because they do not meet the asset recognition criteria.

Under US GAAP, advertising costs are also generally expensed as incurred. However, there are some differences in the timing and method of expensing, and certain costs related to advertising may be capitalized under specific circumstances, unlike IFRS.

Expensing advertising costs as incurred can impact the income statement by reducing net income in the period the costs are incurred. This can affect profitability ratios and potentially influence investment and lending decisions.