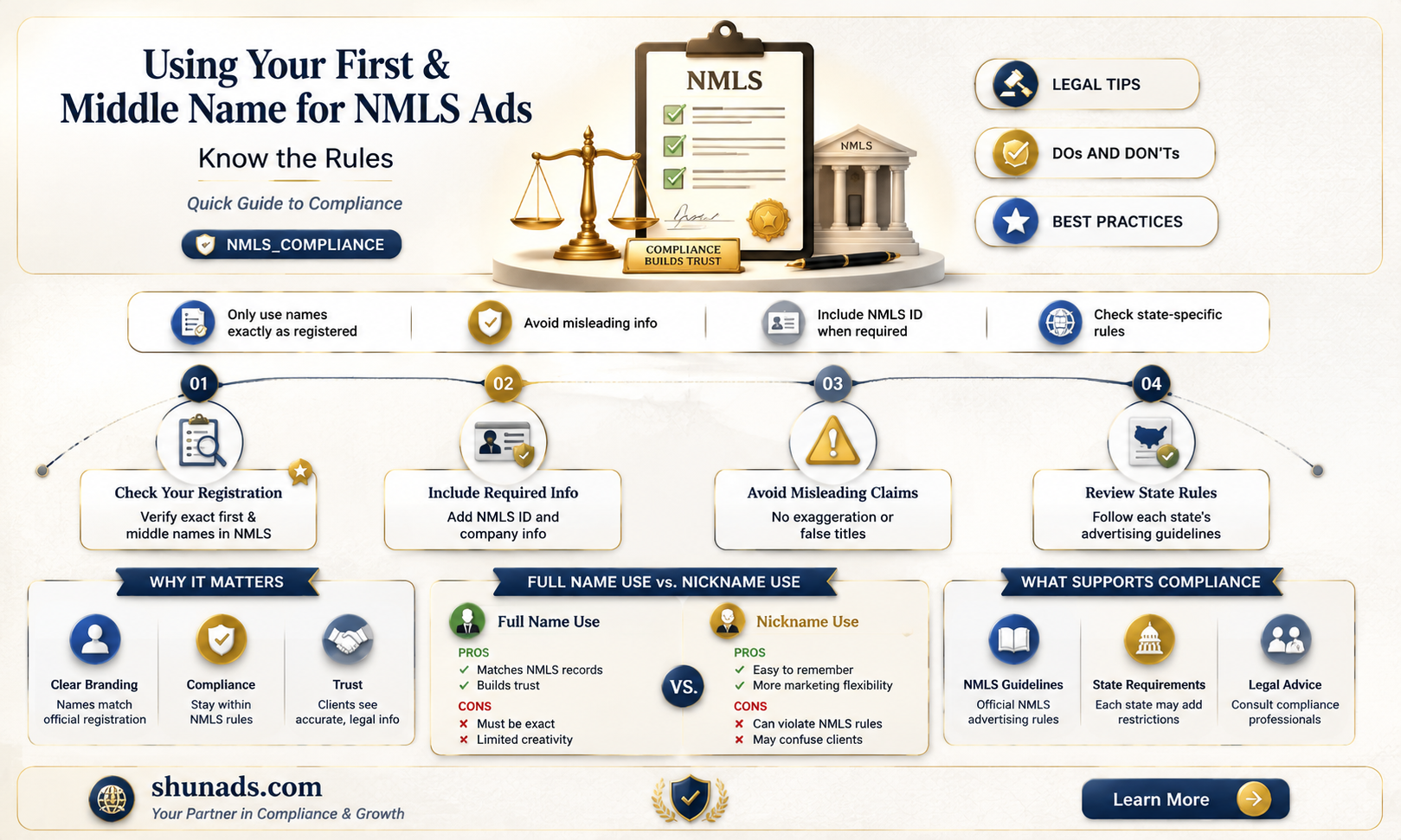

When considering advertising with your first and middle name alongside your NMLS (Nationwide Multistate Licensing System) identifier, it’s essential to understand the regulatory and professional implications. The NMLS requires licensed individuals to use their legal names as registered in the system, ensuring transparency and accountability in financial services. While using your first and middle name may seem straightforward, it’s crucial to verify that this aligns with your NMLS profile and complies with state and federal advertising regulations. Misrepresentation or incomplete information could lead to compliance issues or penalties. Always consult the NMLS Resource Center or legal counsel to ensure your advertising practices meet all necessary standards.

| Characteristics | Values |

|---|---|

| NMLS Requirements | NMLS (Nationwide Multistate Licensing System) regulations do not explicitly prohibit using first and middle names for advertising. However, they emphasize clarity and accuracy in advertising to avoid misleading consumers. |

| Legal Name Usage | Advertising with your first and middle name is generally acceptable if it matches your NMLS-registered name or is a recognized alias. Ensure consistency with your license information. |

| Consumer Confusion | Avoid using names or aliases that could confuse consumers about your identity or affiliation. Clarity is key to compliance. |

| State-Specific Rules | Some states may have additional regulations regarding name usage in advertising. Check state-specific guidelines to ensure compliance. |

| Disclosure Requirements | Always include your full legal name, NMLS ID, and other required disclosures in advertisements, regardless of the name used. |

| Brand vs. Legal Name | If using a brand name or DBA (Doing Business As), ensure it is properly registered and does not misrepresent your identity or services. |

| Enforcement | NMLS and state regulators may take action if advertising is deemed misleading or non-compliant, including fines or license suspension. |

| Best Practice | Use your full legal name or a well-known alias consistently across all advertising materials to maintain transparency and compliance. |

Explore related products

What You'll Learn

- NMLS Name Display Rules: Regulations on using first and middle names in mortgage advertising

- Legal Compliance Tips: Ensuring your ad meets NMLS and state licensing requirements

- Brand Identity Impact: How using partial names affects professional branding in ads

- Consumer Trust Factors: Building credibility with first and middle name advertising

- Penalty Risks: Potential fines or actions for non-compliant name usage in ads

![]()

NMLS Name Display Rules: Regulations on using first and middle names in mortgage advertising

Mortgage professionals often wonder if they can use their first and middle names in advertising while complying with NMLS regulations. The NMLS Name Display Rules are clear: you must use the exact name registered with the Nationwide Multistate Licensing System (NMLS) in all advertising materials. This means if your NMLS registration includes your first and middle name, you can legally use them. However, if your registration only lists your first and last name, adding your middle name could violate compliance standards. Always verify your registered name in the NMLS system before creating ads to avoid penalties.

The rationale behind these rules is to ensure transparency and prevent consumer confusion. By requiring consistent name usage, the NMLS helps borrowers easily identify and verify licensed professionals. For instance, if your NMLS registration is "John Michael Smith," using "J.M. Smith" or "John Smith" in ads could mislead clients. Conversely, if your registered name is "John Smith," adding "Michael" without updating your NMLS profile would be non-compliant. This consistency extends to all marketing channels, including websites, social media, and print materials.

To navigate these rules effectively, follow these steps: First, log into your NMLS account and confirm the exact name listed on your profile. Second, ensure all advertising materials reflect this name verbatim. Third, if you wish to include your middle name, submit a formal name change request through the NMLS system. This process typically takes 7–14 business days, so plan accordingly. Finally, consult with your compliance officer or legal advisor if you’re unsure about specific scenarios, such as using initials or nicknames.

A common pitfall is assuming that personal branding preferences override NMLS regulations. For example, a loan officer named "Mary Elizabeth Johnson" might prefer "Mary E. Johnson" for brevity, but if her NMLS registration is "Mary Johnson," using "E." could trigger compliance issues. Similarly, omitting a middle name to match a DBA (Doing Business As) name is not permitted unless the DBA is also registered with the NMLS. Always prioritize regulatory compliance over branding convenience to avoid fines or license suspension.

In conclusion, while using your first and middle name in mortgage advertising is permissible if it matches your NMLS registration, strict adherence to the rules is non-negotiable. Regularly audit your marketing materials, stay informed about NMLS updates, and proactively address any discrepancies. By doing so, you’ll maintain compliance while effectively promoting your services under your full registered name.

Effective Ways to Remove Annoying Ads in Windows 10

You may want to see also

Explore related products

![]()

Legal Compliance Tips: Ensuring your ad meets NMLS and state licensing requirements

Advertising under your first and middle name in the mortgage industry? It’s a personal touch, but it’s not as simple as slapping your name on a flyer. The NMLS (Nationwide Multistate Licensing System) and state regulators have strict rules to protect consumers and maintain transparency. Ignoring these can lead to fines, license suspension, or worse. Here’s how to stay compliant while leveraging your name in ads.

First, verify your NMLS licensing status. Every ad must include your unique NMLS ID number, clearly and conspicuously. This isn’t optional—it’s a federal requirement. For example, if your name is John Michael Smith and your NMLS ID is 123456, your ad should read: “John Michael Smith, NMLS #123456.” Avoid abbreviations or creative formatting; regulators expect consistency. Pro tip: Double-check your state’s specific rules, as some require additional identifiers like branch licenses.

Next, understand the difference between using your legal name versus a DBA (Doing Business As). If you’re advertising under a DBA, ensure it’s registered with the NMLS and your state. For instance, if John Michael Smith operates as “JMS Mortgage Solutions,” both the DBA and his NMLS ID must appear in the ad. Failure to disclose this can mislead consumers and trigger penalties. Always prioritize clarity over creativity in compliance matters.

Language and disclaimers are another critical area. Ads must avoid misleading claims, such as “guaranteed approval” or “lowest rates.” Instead, use factual, verifiable statements. Include required disclaimers, like “Equal Housing Lender” or state-specific notices. For example, California requires a disclaimer about loan officer licensing. These details may seem minor, but they’re non-negotiable for compliance.

Finally, document everything. Keep records of your ads, including digital and print versions, for at least three years. This isn’t just good practice—it’s often a regulatory requirement. If audited, you’ll need to prove your ads met all NMLS and state standards. Think of it as your compliance safety net. By following these steps, you can advertise with your first and middle name while staying on the right side of the law.

Advertising Vape Products: Legal Challenges and Marketing Strategies Explained

You may want to see also

Explore related products

![NMLS Study Guide 2026-2027 - 5 Full-Length Practice Tests, SAFE MLO Exam Prep Secrets Book for the Mortgage Loan Originator Exam: [4th Edition]](https://m.media-amazon.com/images/I/71wT4iC1dOL._AC_UL320_.jpg)

![NMLS Study Cards: NMLS MLO Test Prep 2025-2026 for the SAFE Mortgage Loan Originator Exam with Practice Test Questions [Full Color Cards]](https://m.media-amazon.com/images/I/61f1NUOp4iL._AC_UL320_.jpg)

![]()

Brand Identity Impact: How using partial names affects professional branding in ads

Using partial names in professional advertising, such as combining your first and middle name with your NMLS identifier, can create a distinctive brand identity. This approach allows you to stand out in a crowded market by offering a memorable, personal touch that differentiates you from competitors who rely on full names or generic branding. For instance, "John Alexander NMLS#123456" is more unique and conversational than "John Doe NMLS#123456," making it easier for clients to recall and associate with your services. However, this strategy requires careful execution to ensure it aligns with regulatory compliance and professional standards.

From a regulatory standpoint, using partial names in ads is generally permissible as long as your NMLS identifier is clearly displayed and your licensing information remains transparent. The NMLS Consumer Access website verifies licensees by full legal names, but advertising guidelines often allow flexibility in how you present your name, provided it’s not misleading. For example, if your legal name is "John Michael Smith," advertising as "John Michael NMLS#123456" is acceptable, but omitting your last name entirely could raise questions about transparency. Always verify state-specific regulations to avoid unintentional violations.

The psychological impact of partial names in branding cannot be overlooked. Combining your first and middle name creates a sense of familiarity and approachability, which can build trust with potential clients. Research shows that names perceived as more "human" or less formal can increase engagement, particularly in industries like mortgage lending, where personal relationships are critical. For instance, "Emily Grace NMLS#123456" feels more relatable than "E.G. Smith NMLS#123456," potentially leading to higher conversion rates. However, this approach may not suit all audiences; older or more traditional clients might prefer formal naming conventions.

To maximize the impact of using partial names, pair this strategy with consistent branding across all platforms. Ensure your partial name and NMLS identifier appear uniformly on business cards, social media profiles, email signatures, and marketing materials. For example, if you advertise as "David James NMLS#123456," maintain this format everywhere to reinforce brand recognition. Additionally, incorporate a tagline or value proposition to clarify your expertise, such as "David James NMLS#123456 – Simplifying Your Mortgage Journey." This combination of personal branding and professional clarity can elevate your visibility and credibility.

Finally, monitor the effectiveness of your partial name branding through analytics and client feedback. Track engagement metrics on ads featuring your partial name versus full name to gauge which resonates more with your target audience. Client testimonials can also provide insights into how your branding influences their perception of trustworthiness and approachability. If feedback suggests confusion or a lack of professionalism, consider adjusting your approach. Ultimately, using partial names in ads is a strategic choice that, when executed thoughtfully, can enhance your professional brand identity while maintaining compliance and authenticity.

Free Ecommerce Advertising: Top Platforms to Promote Your Online Store

You may want to see also

Explore related products

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)

![NMLS SAFE MLO Study Cards 2025-2026: NMLS Exam Prep and Practice Test Questions for Mortgage Loan Originators [Color-Coded]](https://m.media-amazon.com/images/I/51M0L0lQYTL._AC_UL320_.jpg)

![]()

Consumer Trust Factors: Building credibility with first and middle name advertising

Using your first and middle name in advertising as a mortgage loan originator (MLO) can be a powerful way to build consumer trust, but it requires strategic execution. The NMLS (Nationwide Multistate Licensing System) mandates that all advertising include your full legal name and unique identifier, but leveraging your first and middle name goes beyond compliance—it’s about creating a personal connection. Consumers are more likely to trust an individual who presents themselves authentically, as it reduces perceived anonymity and fosters accountability. For example, "John Michael Smith, NMLS #123456" feels more approachable than a generic company name or initials. This approach humanizes your brand, making you memorable in a crowded market.

However, simply adding your first and middle name isn’t enough to build credibility. Pair this tactic with consistent branding across all platforms—business cards, social media, and email signatures. Inconsistency can raise red flags, undermining the trust you’re trying to establish. For instance, if your LinkedIn profile uses only your first name but your email signature includes both, it creates confusion. A cohesive brand identity reinforces reliability, signaling to clients that you’re detail-oriented and professional. Additionally, ensure your NMLS ID is prominently displayed, as it validates your legitimacy and reassures clients they’re working with a licensed professional.

Another critical factor is the tone and content of your messaging. When advertising with your first and middle name, adopt a conversational yet professional tone. Avoid overly formal language that feels distant, but steer clear of casual slang that might diminish your expertise. For example, "Hi, I’m John Michael Smith, and I’m here to guide you through the mortgage process with clarity and care" strikes a balance. Include client testimonials or case studies to back up your personal brand, as third-party validation strengthens credibility. A well-crafted bio or "About Me" section that highlights your experience, values, and commitment to clients can further solidify trust.

Finally, transparency is non-negotiable. While using your first and middle name adds a personal touch, it also invites scrutiny. Be upfront about your services, fees, and limitations. For instance, if you specialize in certain loan types or serve specific demographics, disclose this clearly. Misleading clients, even unintentionally, can erode trust faster than it’s built. Regularly update your advertising materials to reflect any changes in your licensing, services, or contact information. This proactive approach demonstrates integrity and keeps clients confident in your professionalism. By combining authenticity, consistency, and transparency, your first and middle name can become a cornerstone of your credibility in the mortgage industry.

Top Websites for Food Advertising: Boost Your Culinary Brand Online

You may want to see also

Explore related products

![NMLS Study Guide: SAFE Mortgage Loan Originator Test Prep Secrets Book, Full-Length MLO Practice Exam, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71wuD4SQlSL._AC_UL320_.jpg)

![NMLS Study Guide: Practice Tests and MLO SAFE Exam Prep Book for Mortgage Loan Originators: [Includes Detailed Answer Explanations]](https://m.media-amazon.com/images/I/71Fr8rSF1+L._AC_UL320_.jpg)

![]()

Penalty Risks: Potential fines or actions for non-compliant name usage in ads

Using your first and middle name in mortgage advertising without proper NMLS compliance can trigger penalties that range from fines to license revocation. Regulatory bodies like the Consumer Financial Protection Bureau (CFPB) and state regulators enforce strict standards to ensure transparency and prevent consumer confusion. For instance, failing to include your full legal name or NMLS ID in ads may result in fines starting at $5,000 per violation, depending on jurisdiction and severity. Repeat offenders face exponentially higher penalties, making compliance a non-negotiable priority.

Consider the case of a loan officer who advertised using only their first and middle names, omitting their last name and NMLS ID. A routine audit flagged the non-compliance, leading to a $10,000 fine and a mandatory corrective action plan. This example underscores the importance of adhering to NMLS guidelines, which require all advertising materials to include the loan originator’s full name and unique identifier. Ignoring these rules not only risks financial penalties but also damages professional credibility.

To avoid penalties, follow these actionable steps: First, verify your state’s specific advertising requirements, as some states mandate additional disclosures beyond federal rules. Second, ensure all ads—digital, print, or verbal—include your full legal name and NMLS ID in a clear, non-misleading format. Third, regularly audit your marketing materials to catch and correct errors before regulators do. Proactive compliance is far less costly than reactive defense against fines or license suspension.

Comparatively, compliant advertising builds trust with both regulators and clients. A loan officer who consistently includes their full name and NMLS ID in ads not only avoids penalties but also positions themselves as a transparent and trustworthy professional. Conversely, non-compliance signals carelessness or intentional deception, which can alienate clients and invite regulatory scrutiny. The choice between compliance and risk is clear—one fosters growth, while the other invites setbacks.

Finally, treat NMLS compliance as an investment in your career longevity. Penalties for non-compliant name usage extend beyond fines; they can include cease-and-desist orders, mandatory ethics training, or even license revocation. By prioritizing adherence to advertising rules, you protect your livelihood and reputation. Remember, regulators are not just enforcing rules—they’re protecting consumers. Aligning with their standards ensures you remain a trusted participant in the mortgage industry.

Effective Strategies: Where and How to Advertise Your Services Successfully

You may want to see also

Frequently asked questions

Yes, you can advertise using your first and middle name as long as it matches the name on your NMLS license and does not misrepresent your identity or qualifications.

While you can use your first and middle name, it’s generally recommended to include your full legal name, as listed on your NMLS license, to avoid confusion and ensure compliance with regulatory requirements.

There are no explicit restrictions, but using only your first and middle name may require additional clarification to ensure consumers can easily identify you and verify your NMLS credentials.

No, you should use the exact name as it appears on your NMLS license. Using nicknames or abbreviations may violate advertising regulations and cause compliance issues.

![NMLS Study Guide 2024 and 2025: 3 Practice Exams and NMLS SAFE MLO Test Prep: [2nd Edition]](https://m.media-amazon.com/images/I/61eGlPJkVjL._AC_UL320_.jpg)