Chargebacks are typically associated with disputes over financial transactions, where a customer requests a refund from their bank or credit card company due to issues like unauthorized charges, defective products, or services not rendered. However, the question of whether a chargeback can be initiated for false verbal advertising is more complex. Verbal advertising, unlike written or digital ads, often lacks tangible evidence, making it challenging to prove misrepresentation. Chargebacks generally require clear documentation of fraud or breach of contract, which can be difficult to establish with verbal claims alone. While consumers may feel misled by false verbal advertising, chargebacks are typically not the appropriate recourse in such cases. Instead, addressing the issue directly with the merchant or seeking legal advice may be more effective avenues for resolution.

Explore related products

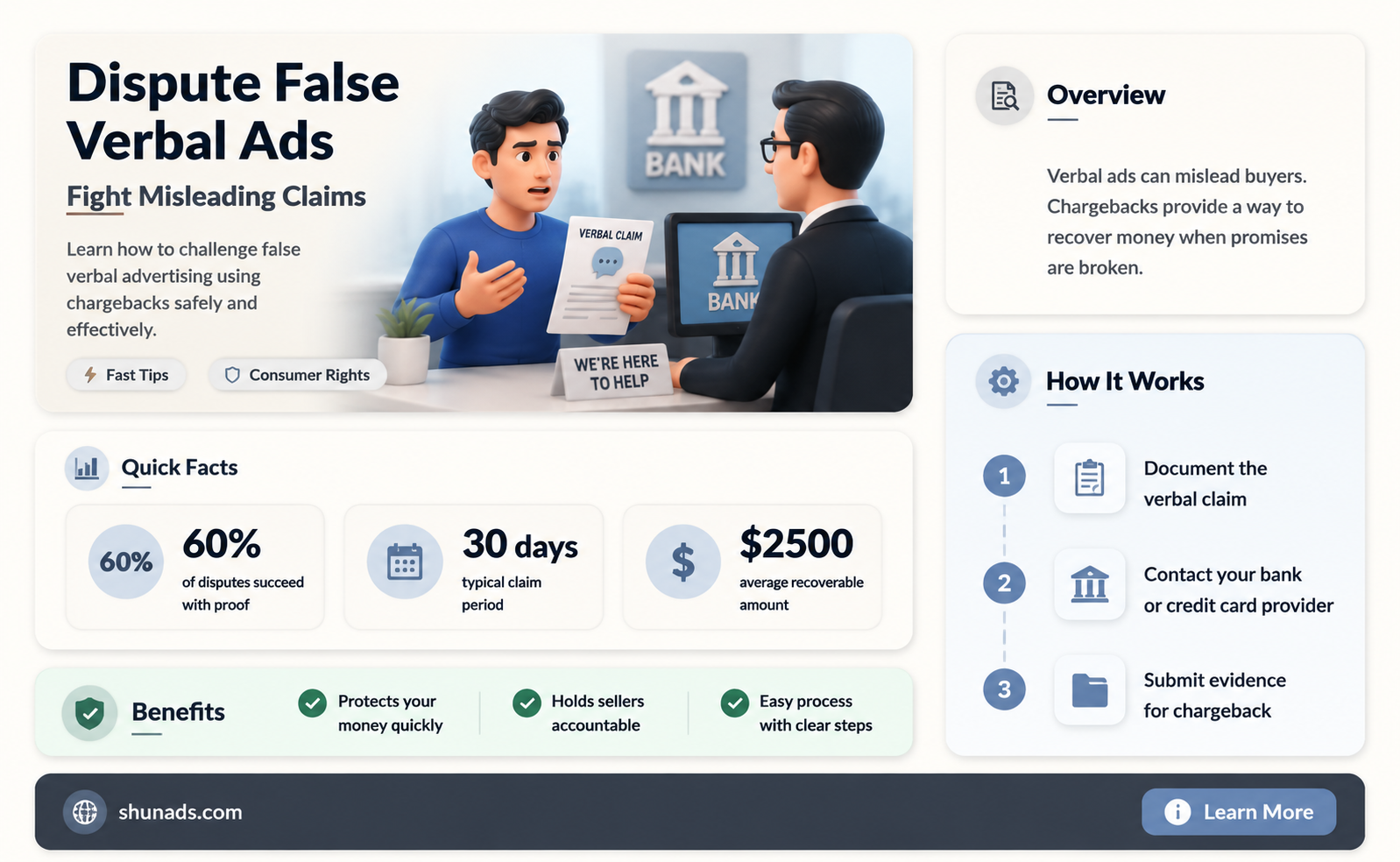

What You'll Learn

![]()

Understanding False Advertising Claims

False advertising claims hinge on the disparity between what’s promised and what’s delivered. Verbal advertisements, though less tangible than written ones, are still legally binding in many jurisdictions. For instance, if a salesperson claims a product will "eliminate 99% of allergens" but it fails to perform as stated, this could constitute false advertising. The challenge lies in proving the exact nature of the verbal claim, as it often relies on memory or witness testimony. Always document conversations, noting dates, times, and specific statements made by the advertiser. This evidence becomes critical if you pursue a chargeback or legal action.

Proving false verbal advertising requires more than just dissatisfaction with a product or service. You must demonstrate that the advertiser made a specific, misleading claim that directly influenced your purchase decision. For example, if a gym salesperson guarantees "unlimited access" but later restricts hours, this could be grounds for a claim. Financial institutions and consumer protection agencies typically require clear evidence of the misrepresentation, such as a recording (where legal) or corroborating witnesses. Without concrete proof, chargebacks for verbal claims are often denied, as they rely heavily on the cardholder’s word against the merchant’s.

Chargebacks for false verbal advertising are possible but fraught with challenges. Most credit card companies and banks follow the Fair Credit Billing Act (FCBA), which allows chargebacks for goods or services not delivered as agreed. However, verbal agreements are harder to enforce than written contracts. To increase your chances, act promptly—most banks require disputes within 60 days of the purchase. Provide detailed documentation, including the exact claim made, the date of the transaction, and any attempts to resolve the issue directly with the merchant. Be prepared for the merchant to dispute your claim, as they often have more resources to fight chargebacks.

A comparative analysis reveals that written advertisements are easier to challenge than verbal ones due to their permanence. For instance, a misleading online ad can be screenshot and submitted as evidence, whereas a verbal claim often boils down to he-said-she-said scenarios. However, some jurisdictions, like the U.S. Federal Trade Commission (FTC), treat verbal and written claims equally under the FTC Act, which prohibits unfair or deceptive practices. If you’re in a region with strong consumer protection laws, consult local agencies for guidance. For example, the UK’s Consumer Rights Act 2015 covers both written and verbal misrepresentations, offering a clearer path to redress.

To protect yourself from false verbal advertising, adopt proactive measures. Always ask for written confirmation of any verbal claims, especially for high-value purchases. If the merchant refuses, consider walking away from the deal. For ongoing services, such as subscriptions or memberships, review cancellation policies before signing up. Keep all receipts and correspondence, as these can support your case if a dispute arises. Finally, familiarize yourself with your credit card’s chargeback policy and the local consumer protection laws. While chargebacks for verbal claims are challenging, understanding your rights and gathering solid evidence can tip the scales in your favor.

Canada's Free Land Offer: Unsettled Promises and Lasting Legacies

You may want to see also

Explore related products

![]()

Chargeback Eligibility for Verbal Misrepresentation

Verbal misrepresentation in advertising can leave consumers feeling deceived, but does it qualify for a chargeback? The answer hinges on proving the discrepancy between what was promised and what was delivered. Chargebacks are typically designed to address tangible issues like unauthorized charges or undelivered goods, but they can sometimes extend to cases where verbal claims directly contradict the product or service received. For instance, if a salesperson guarantees a car’s fuel efficiency at 40 mpg, but the actual performance is 25 mpg, this could be grounds for a chargeback if documented evidence supports the claim.

To pursue a chargeback for verbal misrepresentation, documentation is your strongest ally. While verbal agreements are harder to prove, any written materials, recordings, or witnesses can bolster your case. For example, if a fitness coach verbally promises a 30-day money-back guarantee but refuses to honor it, emails, text messages, or even a contract mentioning the guarantee can serve as evidence. Without such proof, credit card companies or banks may be reluctant to process the chargeback, as they rely on concrete evidence to determine eligibility.

The success of a chargeback for verbal misrepresentation also depends on the payment method and the issuer’s policies. Credit card companies like Visa or Mastercard have specific dispute categories, such as “goods/services not as described,” which can apply if verbal claims were materially different from reality. However, debit card chargebacks or disputes through platforms like PayPal may have stricter criteria. Always review the dispute policies of your payment provider and act promptly, as most chargebacks must be initiated within 120 days of the transaction.

A cautionary note: chargebacks should not be the first step. Attempt to resolve the issue directly with the merchant before escalating. Many businesses are willing to rectify mistakes or miscommunications to avoid a formal dispute. If negotiations fail, contact your bank or credit card company with clear, concise documentation. Be prepared to explain how the verbal misrepresentation directly impacted the value or functionality of the product or service, as this will strengthen your case.

In conclusion, while chargebacks for verbal misrepresentation are possible, they require careful preparation and evidence. Focus on gathering proof, understanding your payment provider’s policies, and exhausting direct resolution attempts before proceeding. By approaching the process strategically, you can increase your chances of a successful outcome and protect yourself from deceptive practices.

Advertising Without a License: Who Can Legally Promote Services?

You may want to see also

Explore related products

![]()

Evidence Required for Dispute

Initiating a chargeback for false verbal advertising hinges on concrete evidence, as verbal claims alone rarely suffice. Unlike written advertisements, verbal promises are ephemeral, making proof challenging. To build a compelling case, start by documenting every interaction with the seller. Record dates, times, and names of representatives involved. If possible, obtain a written summary of the verbal agreement or advertisement immediately after the conversation. This creates a tangible record that can be referenced later. Without such documentation, your claim may lack the foundation needed to convince your bank or credit card issuer.

The strength of your evidence lies in its ability to demonstrate a clear discrepancy between what was promised and what was delivered. For instance, if a salesperson claimed a product had specific features or capabilities, gather product manuals, specifications, or expert opinions that contradict these claims. Screenshots of online reviews or testimonials that align with your experience can also bolster your case. If the transaction involved a service, document the lack of fulfillment through emails, photos, or witness statements. The goal is to create a narrative that is both detailed and irrefutable.

While verbal evidence is inherently weaker, pairing it with circumstantial proof can significantly enhance your position. For example, if the false advertisement occurred during a recorded call, request access to the recording from the company. If denied, note this refusal in your dispute documentation, as it may reflect poorly on the merchant’s transparency. Similarly, if multiple customers experienced the same issue, compile their accounts to demonstrate a pattern of misleading behavior. This collective evidence can shift the burden of proof onto the merchant, compelling them to justify their actions.

Finally, understand the limitations of your evidence and the chargeback process. Banks and credit card companies typically prioritize written agreements and tangible proof over verbal claims. If your evidence is primarily circumstantial, consider supplementing it with a formal complaint to consumer protection agencies or legal advice. While chargebacks are a powerful tool, they are not a guaranteed solution for every dispute. By meticulously gathering and presenting your evidence, you maximize your chances of a favorable outcome while setting a precedent for accountability in verbal advertising practices.

Leveraging IP Address Data for Targeted Advertising Strategies and Campaigns

You may want to see also

Explore related products

![]()

Steps to File a Chargeback

False verbal advertising can leave you feeling deceived and financially harmed. If you've fallen victim to misleading promises, a chargeback might be your recourse. Here's a breakdown of the steps involved, along with crucial considerations:

- Gather Your Evidence: Treat this like a detective work. Document everything related to the transaction: receipts, emails, screenshots of advertisements, recordings of phone calls (if legal in your jurisdiction), and any written communication with the merchant. Note down dates, times, and the specific claims made verbally that were not fulfilled. The stronger your evidence, the stronger your case.

- Contact the Merchant First: Before initiating a chargeback, attempt to resolve the issue directly with the merchant. Clearly explain the discrepancy between the verbal advertisement and the reality, and request a refund or appropriate remedy. Keep a record of all communication attempts. Many merchants are willing to rectify mistakes to avoid the hassle of a chargeback.

- Understand Your Rights and Time Limits: Chargeback rules vary depending on your payment method (credit card, debit card, PayPal, etc.) and your location. Familiarize yourself with the specific policies of your card issuer or payment processor. Typically, you have a limited timeframe (usually 60-120 days) from the transaction date to file a chargeback.

- Initiate the Chargeback Process: Contact your bank or credit card company and clearly state your intention to file a chargeback. Provide them with all the evidence you've gathered, including a detailed explanation of the false advertising and your attempts to resolve the issue with the merchant. Be prepared to answer questions and provide additional documentation if requested.

- Be Prepared for the Merchant's Response: The merchant will have the opportunity to dispute your chargeback. They may provide counter-evidence or argue that the advertisement was not misleading. Remain patient and cooperative throughout the process, providing any additional information requested by your bank or card issuer.

Remember, chargebacks are a serious matter and should be used responsibly. Only pursue a chargeback if you have strong evidence of false advertising and have exhausted all other avenues for resolution. Misusing chargebacks can damage your relationship with your bank and potentially lead to penalties.

Free Newsletter Promotion: Top Platforms to Advertise at No Cost

You may want to see also

Explore related products

$47.99

![]()

Legal Alternatives to Chargebacks

Chargebacks are often seen as a quick remedy for disputes over false advertising, but they come with risks like account penalties or legal backlash. Before resorting to this nuclear option, explore legal alternatives that are both effective and less confrontational. Start by documenting every detail of the verbal advertisement—date, time, person involved, and specific claims made. This evidence will be crucial if you escalate the issue.

One powerful alternative is leveraging consumer protection laws. In the U.S., the Federal Trade Commission (FTC) enforces regulations against deceptive advertising. File a complaint with the FTC online or by phone, providing all documented evidence. Similarly, in the EU, the Unfair Commercial Practices Directive offers recourse for misleading claims. Local consumer protection agencies can also intervene on your behalf, often resolving disputes without legal fees. These agencies have the authority to mediate, demand refunds, or even penalize the business.

Another strategic move is to engage the business directly through a formal demand letter. Draft a concise, professional letter outlining the false claims, their impact, and your desired resolution (e.g., refund, correction, or compensation). Include a deadline for response, typically 14–30 days. A well-crafted letter often prompts businesses to act to avoid further scrutiny. If they refuse, this letter becomes evidence of bad faith, strengthening your case in small claims court.

For disputes under $10,000, small claims court is a cost-effective option. Unlike chargebacks, which rely on banks, this route lets you argue your case directly to a judge. Prepare by organizing all evidence, including recordings (if legal in your state), emails, and witness statements. Many courts offer self-help resources or workshops to guide you through the process. While it requires more effort, the outcome is binding and can include compensation beyond a refund.

Finally, consider industry-specific dispute resolution bodies. For instance, telecom or travel industries often have ombudsmen or regulatory bodies that handle consumer complaints. These entities can investigate and enforce compliance, sometimes awarding compensation. Check if the business belongs to trade associations with dispute resolution mechanisms. This approach is particularly useful when dealing with niche industries or international transactions where local laws may not apply.

By exhausting these legal alternatives, you not only avoid the pitfalls of chargebacks but also contribute to holding businesses accountable for false advertising. Each step builds a stronger case, ensuring you’re prepared if further action is needed.

Get Paid to Advertise for Amazon: A Profitable Side Hustle

You may want to see also

Frequently asked questions

Yes, you may be able to initiate a chargeback if a merchant made false verbal claims that significantly misrepresented the product or service, and you can provide evidence of the misrepresentation.

Evidence may include witness statements, recordings (if legal in your jurisdiction), correspondence with the merchant, or any documentation that proves the verbal claims were false and misleading.

Approval depends on the strength of your evidence and the policies of your bank or credit card company. Chargebacks for verbal claims are often more challenging to prove, so it’s important to provide clear and compelling documentation.