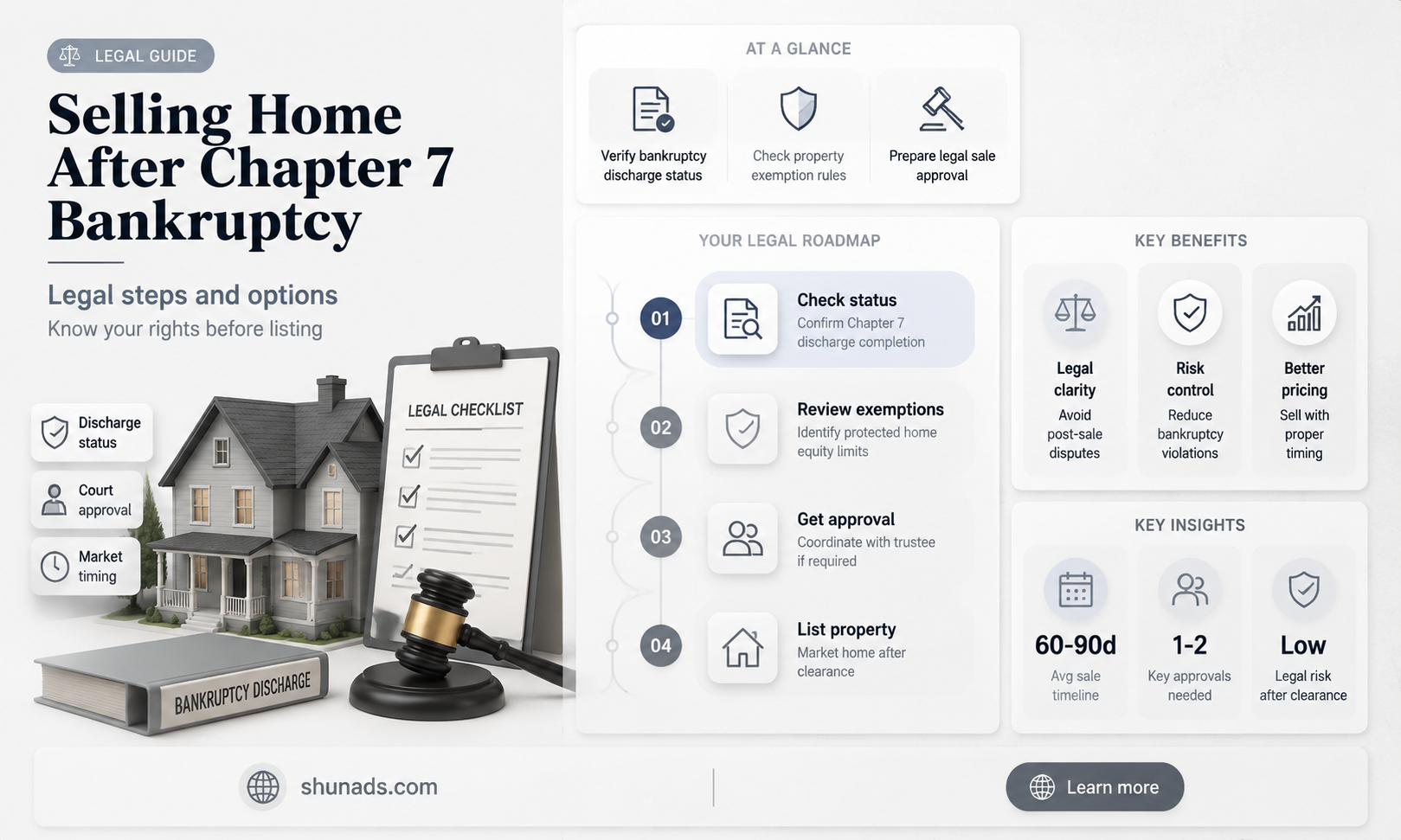

After filing for Chapter 7 bankruptcy, many homeowners wonder about the implications for their property, particularly whether their house can still be advertised for sale. Chapter 7 bankruptcy typically involves liquidating assets to pay off creditors, but if the house is protected by exemptions or has no equity, it may not be sold. However, if the house is part of the bankruptcy estate, the trustee can list and sell it to satisfy debts. Even if the house is exempt, homeowners may still choose to sell it voluntarily to improve their financial situation. Importantly, advertising the house for sale after Chapter 7 depends on whether the property is part of the bankruptcy estate or if the homeowner retains ownership post-discharge. Consulting with a bankruptcy attorney is crucial to understand the specific circumstances and legal options.

| Characteristics | Values |

|---|---|

| Chapter 7 Bankruptcy | A legal process where a debtor's assets are liquidated to pay off creditors, and any remaining eligible debts are discharged. |

| House Ownership Post-Chapter 7 | If the house is exempt from liquidation (due to state exemptions or no equity), the homeowner retains ownership after bankruptcy discharge. |

| Advertising the House | If the house is retained post-Chapter 7, the homeowner can choose to advertise and sell it, as it is no longer part of the bankruptcy estate. |

| Trustee's Role | The bankruptcy trustee can advertise and sell the house only if it was part of the bankruptcy estate and not exempt. After discharge, the trustee no longer has control over exempt property. |

| Exemptions | State-specific homestead exemptions determine if the house is protected from liquidation. If exempt, it cannot be advertised or sold by the trustee. |

| Post-Discharge Rights | After Chapter 7 discharge, the homeowner regains full control over exempt property, including the right to advertise and sell the house. |

| Creditor Claims | If the house was not liquidated during bankruptcy, creditors cannot force its sale or advertising post-discharge, as eligible debts are discharged. |

| Reaffirmation Agreement | If the homeowner reaffirms the mortgage debt, they remain responsible for payments but retain the right to advertise and sell the house. |

| Tax Implications | Selling the house post-Chapter 7 may have tax consequences, such as capital gains tax, depending on the sale price and exemptions used. |

| Legal Advice | Consulting a bankruptcy attorney is recommended to understand specific state laws and exemptions regarding advertising and selling a house post-Chapter 7. |

Explore related products

What You'll Learn

![]()

Legal Restrictions Post-Chapter 7

After filing for Chapter 7 bankruptcy, the legal restrictions surrounding your property, including your house, become a critical area of focus. One of the most pressing questions homeowners face is whether creditors or real estate agents can advertise their house post-bankruptcy. The answer lies in understanding the automatic stay and the discharge injunction, two legal protections that come into play during and after Chapter 7 proceedings. The automatic stay immediately halts most collection actions, including foreclosure and property advertisements, upon filing for bankruptcy. However, once the discharge is granted, the discharge injunction permanently bars creditors from pursuing discharged debts, but its impact on property advertising is nuanced.

To navigate this complexity, consider the following steps. First, verify whether your house was included in the bankruptcy estate. If it was exempted and retained, creditors generally cannot advertise it for sale without violating the discharge injunction. Second, review the terms of your bankruptcy discharge to ensure no liens or claims remain on the property. If a creditor still holds a valid lien, they might attempt to advertise the house as part of a foreclosure process, though this would require court approval post-discharge. Practical tip: consult your bankruptcy attorney to confirm the status of your property and any lingering obligations.

A comparative analysis reveals that Chapter 7 differs significantly from Chapter 13 in this regard. In Chapter 13, the debtor often retains control of their property while repaying debts over time, reducing the likelihood of post-bankruptcy advertising. Chapter 7, however, involves liquidation of non-exempt assets, which might lead creditors to believe they can advertise property prematurely. This misconception underscores the importance of understanding the discharge injunction’s scope—it prohibits actions to collect discharged debts, including advertising property tied to such debts. Example: If a second mortgage was discharged, the lender cannot advertise the house to recover the debt, as doing so would violate federal law.

Persuasively, homeowners must assert their rights under the Bankruptcy Code if creditors attempt to advertise their house post-Chapter 7. Document all communications and report violations to the bankruptcy court. Creditors found in violation may face sanctions, including fines or contempt charges. Takeaway: While the discharge injunction provides robust protection, vigilance and legal knowledge are essential to prevent unauthorized property advertisements. Always keep records of your bankruptcy discharge and consult legal counsel if issues arise.

Cutting Ad Spend: Can Pharma Companies Reduce Marketing Investments?

You may want to see also

Explore related products

![]()

Realtor’s Role in Advertising

After filing for Chapter 7 bankruptcy, homeowners often face uncertainty about the fate of their property. A critical question arises: Can a realtor advertise your house during or after this process? The answer lies in understanding the legal boundaries and strategic opportunities that emerge post-bankruptcy. Realtors play a pivotal role in navigating these complexities, ensuring compliance while maximizing the property’s market potential.

Step 1: Assess the Bankruptcy Trustee’s Authority

Once Chapter 7 is filed, the bankruptcy trustee gains control over non-exempt assets, including real estate. Realtors must coordinate with the trustee to determine if the property can be listed. Advertising without approval risks legal complications. For instance, if the trustee decides to sell the property to repay creditors, the realtor’s role shifts to facilitating the trustee’s sale rather than initiating independent marketing efforts.

Caution: Avoid Misrepresentation

Realtors must be transparent in their advertising. Phrases like “bankruptcy sale” or “distressed property” can attract buyers but must be used ethically. Misleading claims about the property’s status or pricing violate real estate regulations and ethical standards. For example, stating “below market value” without evidence could lead to disputes or legal action.

Strategic Advertising Post-Discharge

After the bankruptcy discharge, if the homeowner retains the property, realtors can employ targeted strategies. Highlighting the property’s unique features, such as location or recent renovations, shifts focus away from its financial history. Utilizing platforms like Zillow, social media, and local listings can attract a broader audience. For instance, a realtor might emphasize a home’s proximity to schools or its energy-efficient upgrades to appeal to families or eco-conscious buyers.

Collaborate with Legal Professionals

Realtors should advise clients to consult bankruptcy attorneys before listing. This ensures all legal obligations are met and prevents post-sale complications. For example, if a creditor disputes the sale, having legal documentation in place protects both the homeowner and the realtor. A proactive approach minimizes risks and builds trust with clients navigating financial recovery.

In summary, a realtor’s role in advertising a house after Chapter 7 hinges on legal compliance, strategic marketing, and ethical transparency. By understanding the trustee’s authority, avoiding misrepresentation, and leveraging post-discharge opportunities, realtors can effectively guide clients through this challenging process. Practical steps, such as collaborating with legal professionals and focusing on property strengths, ensure a smooth and successful sale.

Can the BBB Sue for False Advertising? Legal Insights Explained

You may want to see also

Explore related products

![]()

Impact on Property Value

Filing for Chapter 7 bankruptcy can have a profound and multifaceted impact on your property value, often in ways that aren’t immediately apparent. One critical factor is the stigma associated with bankruptcy itself. Prospective buyers may perceive a property previously tied to financial distress as less desirable, even if the home’s physical condition remains unchanged. This psychological barrier can lead to lower offers or prolonged time on the market, effectively depressing the property’s market value. Real estate agents often report that homes with a bankruptcy history require strategic pricing and marketing to counteract this bias.

Another layer of complexity arises from the legal process itself. If a house is advertised post-Chapter 7, it may still be subject to liens or unresolved claims that weren’t discharged in bankruptcy. These encumbrances can deter buyers, as they may fear inheriting unexpected liabilities. For instance, a lingering tax lien or a creditor’s claim could cloud the title, making it harder to secure financing or complete the sale. Sellers must conduct a thorough title search and disclose all potential issues to avoid legal complications down the line.

From a comparative perspective, properties advertised after Chapter 7 often face unfair competition from similar homes without such a history. Buyers typically prioritize "clean" transactions, and a bankruptcy-linked property may be overlooked in favor of alternatives with simpler ownership histories. This dynamic can force sellers to reduce their asking price by 5–10% to remain competitive, depending on local market conditions. In regions with high inventory, the discount may need to be even steeper to attract serious offers.

To mitigate these effects, sellers should focus on proactive strategies. First, invest in minor renovations or staging to highlight the property’s best features, shifting the narrative away from its financial history. Second, work with an experienced real estate attorney to ensure all legal hurdles are cleared before listing. Finally, consider targeting cash buyers or investors who are less likely to be deterred by the property’s past. While Chapter 7 can cast a long shadow, thoughtful preparation and positioning can help restore a property’s market appeal.

Effective Advertising Strategies to Promote Your Photography Business Online & Offline

You may want to see also

Explore related products

![]()

Timeline for Listing Post-Bankruptcy

After filing for Chapter 7 bankruptcy, the timeline for listing your house hinges on the discharge of your debts and the trustee’s handling of your assets. Typically, the bankruptcy process takes about 3–4 months from filing to discharge. During this period, the court-appointed trustee evaluates your property, including your home, to determine if it can be sold to repay creditors. If your home has equity exceeding your state’s homestead exemption, the trustee may liquidate it. However, if the equity is protected, the trustee will likely abandon the property, allowing you to retain it. Once the discharge is granted, you regain control over your assets, and the timeline for listing your house shifts to your personal circumstances and market conditions.

Assuming the trustee abandons your home, the next step involves assessing your financial readiness to sell. Post-bankruptcy, your credit score may have taken a hit, but selling your house can provide a fresh start by eliminating a major liability. Before listing, consult a real estate attorney to ensure all legal obligations are met, such as clearing any lingering liens or judgments. Additionally, work with a realtor who understands post-bankruptcy sales to navigate potential challenges, such as buyer skepticism about your financial history. The ideal timeline for listing is 1–2 months after discharge, giving you time to prepare the property and market it effectively without rushing.

Market conditions play a critical role in determining the optimal listing timeline. In a seller’s market, where demand outpaces supply, you may benefit from listing immediately post-discharge to capitalize on high prices and quick sales. Conversely, in a buyer’s market, waiting a few months to improve your home’s curb appeal or make minor repairs could yield a better return. Use tools like comparative market analyses (CMAs) to gauge local trends and price your home competitively. Remember, post-bankruptcy, transparency is key—disclose the bankruptcy to potential buyers to avoid legal complications later.

Finally, consider the emotional and logistical aspects of selling post-bankruptcy. Downsizing or relocating can be stressful, so plan your move carefully to avoid overlapping expenses. Allocate 2–3 months for packing, finding a new residence, and coordinating the sale. If you’re renting after selling, factor in security deposits and first-month rent into your budget. By aligning your listing timeline with your personal and financial recovery, you can turn the sale of your home into a stepping stone toward rebuilding your financial stability.

Unveiling Advertiser Bias: Strategies to Enhance Critical Awareness

You may want to see also

Explore related products

![]()

Disclosure Requirements to Buyers

After filing for Chapter 7 bankruptcy, a common concern for homeowners is whether their house can be advertised for sale. While the bankruptcy process may discharge certain debts, it doesn't automatically erase the obligation to disclose relevant information to potential buyers. In fact, disclosure requirements become even more critical in this scenario, as buyers have the right to know about the property's history, including any bankruptcy filings.

One key aspect of disclosure is the requirement to reveal any defects or issues with the property that may affect its value or desirability. This includes structural problems, environmental hazards, or pending legal disputes. In the context of Chapter 7 bankruptcy, sellers must also disclose the fact that the property was part of the bankruptcy estate. This information is typically included in the seller's disclosure statement, which is a legal document that outlines the property's condition and history. Failure to disclose this information can result in legal consequences, including rescission of the sale or damages awarded to the buyer.

From a practical standpoint, it's essential to understand the specific disclosure requirements in your state or jurisdiction. Some states have mandatory disclosure forms that must be completed and provided to buyers, while others may require a more general disclosure statement. In general, sellers should err on the side of caution and disclose any information that may be relevant to the buyer's decision-making process. This includes not only the bankruptcy filing but also any other factors that may affect the property's value, such as pending foreclosures, tax liens, or other encumbrances.

A comparative analysis of disclosure requirements across different states reveals varying levels of stringency. For instance, some states, like California, have comprehensive disclosure laws that require sellers to provide detailed information about the property's condition, including any known defects or hazards. In contrast, other states may have more lenient requirements, allowing sellers to disclose information on a more voluntary basis. However, even in states with less stringent disclosure laws, sellers can still be held liable for nondisclosure or misrepresentation of material facts. As a general rule, it's advisable to consult with a real estate attorney or agent to ensure compliance with local disclosure requirements and to minimize the risk of legal disputes.

To navigate the disclosure process effectively, sellers can follow a few practical steps. First, gather all relevant documentation, including the bankruptcy filing, discharge papers, and any other records related to the property. Next, review the disclosure requirements in your state and complete the necessary forms or statements. Be thorough and accurate in your disclosures, and consider attaching supporting documentation to provide additional context. Finally, work closely with your real estate agent or attorney to ensure that the disclosure information is presented clearly and prominently to potential buyers. By taking a proactive and transparent approach to disclosure, sellers can build trust with buyers and reduce the risk of legal complications down the line.

Sponsorships as Advertising: Tax Deduction Eligibility Explained

You may want to see also

Frequently asked questions

Yes, a real estate agent can still advertise your house after you file for Chapter 7 bankruptcy, but the sale of the property will be subject to court approval and the terms of your bankruptcy case.

Filing Chapter 7 bankruptcy will not automatically stop the advertising of your house, but the sale process will be paused until the bankruptcy court decides how to handle the property.

You can continue to advertise your house during the Chapter 7 process, but any offers or sales must be approved by the bankruptcy trustee and court.

Chapter 7 bankruptcy may discharge personal liability for advertising costs, but the trustee will determine if the expenses are necessary for the sale of the property.

Yes, the bankruptcy trustee has the authority to take control of your assets, including your house, and can advertise and sell it as part of the bankruptcy estate without your consent.