When advertising rental properties, landlords and property managers often consider including specific requirements to attract suitable tenants. One common question that arises is whether it is legal or advisable to post a minimum credit score in rental advertisements. This practice can be a double-edged sword, as it may help streamline the tenant screening process by attracting applicants who meet the desired financial criteria, but it also raises concerns about potential discrimination and compliance with fair housing laws. Understanding the legal and ethical implications of disclosing a minimum credit score requirement is essential for landlords to ensure they are operating within the bounds of the law while effectively managing their rental properties.

| Characteristics | Values |

|---|---|

| Legality | Varies by jurisdiction; some states/countries prohibit it, others allow it |

| Fair Housing Act (U.S.) | May violate the Act if it disproportionately impacts protected classes |

| Purpose | To screen tenants based on financial responsibility |

| Common Practice | Increasingly used by landlords and property managers |

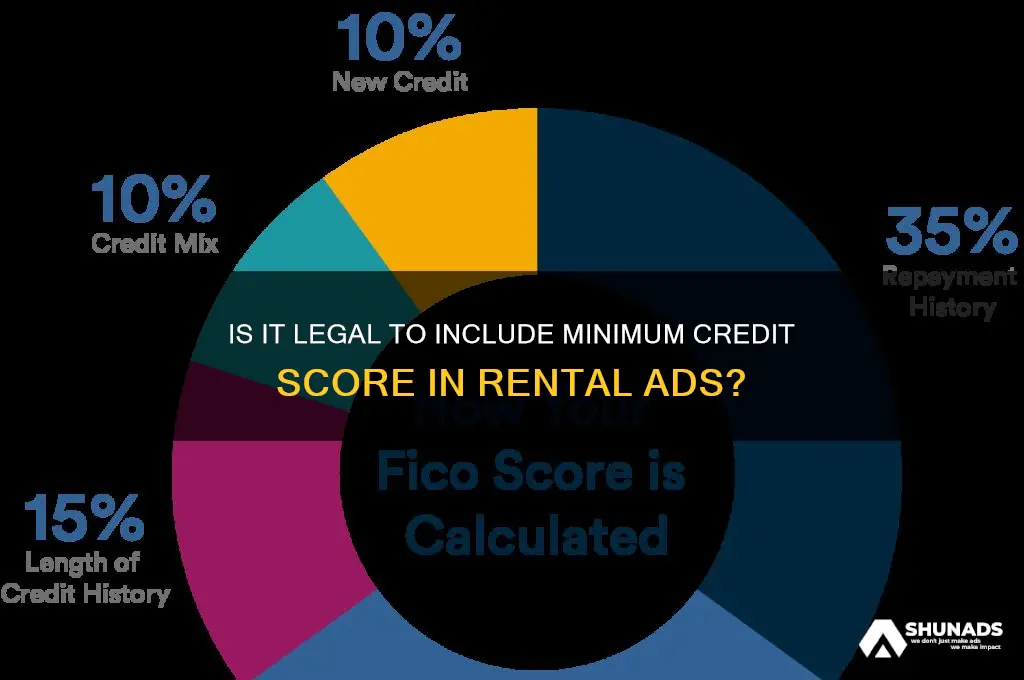

| Minimum Credit Score Range | Typically 600–650, but varies by landlord/property |

| Alternative Screening Methods | Income verification, rental history, references, co-signers |

| Potential Discrimination Concerns | May disproportionately affect low-income or minority applicants |

| Transparency Requirements | Must disclose credit score criteria if used in screening |

| Tenant Rights | Tenants can dispute inaccurate credit information |

| Impact on Tenant Pool | May limit applicants with lower credit scores |

| Legal Alternatives | Use credit reports without specifying a minimum score |

| State-Specific Regulations | Some states (e.g., California) restrict credit-based screening |

| Landlord Risks | Potential lawsuits if deemed discriminatory |

| Industry Trends | Growing use of holistic tenant screening tools |

| Tenant Advocacy | Organizations push for fairer screening practices |

Explore related products

What You'll Learn

![]()

Legal Implications of Credit Score Requirements

Credit score requirements in rental advertisements, while seemingly straightforward, carry significant legal implications that landlords and property managers must navigate carefully. Federal and state laws, such as the Fair Housing Act (FHA) and the Fair Credit Reporting Act (FCRA), impose strict guidelines on how credit scores can be used in tenant screening. For instance, the FHA prohibits discriminatory practices based on race, color, religion, sex, familial status, national origin, or disability. If a credit score requirement disproportionately impacts protected classes—even unintentionally—it could be deemed discriminatory. Landowners must ensure their policies are consistently applied and justified by business necessity to avoid legal challenges.

One critical aspect is the adverse action notice required under the FCRA. If a landlord denies an applicant based on their credit score, they must provide a written notice explaining the decision, including the specific credit score used and the source of the credit report. Failure to comply can result in penalties, including fines and lawsuits. Additionally, some states, like California, have enacted laws limiting the use of credit scores in tenant screening altogether, further complicating compliance. Landlords must stay informed about local regulations to avoid inadvertently violating the law.

Another legal pitfall arises from the disparate impact doctrine, which holds that seemingly neutral policies can still be unlawful if they disproportionately harm protected groups. For example, a minimum credit score requirement might disproportionately exclude applicants from minority communities, who statistically have lower credit scores due to systemic inequalities. To mitigate this risk, landlords should consider alternative screening methods, such as rental history or income verification, alongside credit scores. Documenting the business necessity of credit score requirements and regularly reviewing their impact can provide a legal safeguard.

Practical tips for landlords include standardizing the screening process to ensure fairness and consistency. Clearly outline the criteria used in rental advertisements, avoiding vague or overly restrictive language. For instance, instead of stating a rigid minimum credit score, consider phrasing like "creditworthiness will be evaluated as part of the application process." This approach provides flexibility while maintaining transparency. Additionally, consult legal counsel to draft compliant rental policies and stay updated on evolving laws.

In conclusion, while credit score requirements can be a useful tool for assessing tenant reliability, they are not without legal risks. Landlords must balance their screening needs with compliance obligations to avoid costly litigation and reputational damage. By understanding the legal landscape, implementing fair practices, and staying proactive, property managers can navigate this complex area effectively.

Pocket Listing Advertising Duration: Maximizing Exposure Without Overstepping Boundaries

You may want to see also

Explore related products

![]()

Fair Housing Act Compliance

Advertising a minimum credit score in rental listings may seem like a straightforward way to screen tenants, but it’s a practice that demands careful scrutiny under the Fair Housing Act (FHA). The FHA prohibits discrimination based on race, color, religion, sex, familial status, national origin, or disability. While credit scores themselves aren’t protected classes, their application can disproportionately impact certain groups, raising red flags for potential disparate impact claims. For instance, studies show that minorities and low-income individuals often have lower credit scores due to systemic barriers, such as limited access to credit or predatory lending practices. By imposing a blanket credit score requirement, landlords risk inadvertently excluding these protected groups, even if discrimination isn’t intentional.

To navigate this legally, landlords must ensure that any credit score requirement is both necessary and directly related to the tenant’s ability to fulfill lease obligations. This means the policy should be consistently applied and backed by evidence demonstrating its relevance to tenancy risks. For example, a landlord might justify a minimum credit score by showing data linking lower scores to higher eviction rates in their specific rental market. However, relying solely on credit scores without considering other factors, such as income or rental history, weakens this justification. The FHA requires a balanced approach, encouraging landlords to use credit scores as one of several screening tools rather than a rigid cutoff.

A practical strategy for compliance is to adopt a two-tiered screening process. First, establish a minimum credit score threshold, but pair it with flexibility. For applicants who fall below the threshold, offer alternatives, such as requiring a larger security deposit, a co-signer, or proof of stable income. This approach not only mitigates legal risks but also broadens the pool of qualified tenants. Additionally, landlords should document their reasoning for any denials, ensuring decisions are based on objective criteria rather than subjective judgments. Transparency in the screening process builds trust and reduces the likelihood of FHA violations.

Another critical aspect of compliance is clear communication in rental advertisements. Instead of stating a hard minimum credit score, consider phrasing such as, “Credit history will be considered as part of the application process.” This language avoids deterring protected groups while still signaling that financial responsibility is a factor. Including a disclaimer about alternative screening options can further demonstrate a commitment to fairness. For example, “Applicants with varying credit backgrounds are encouraged to apply; alternative qualifications may be considered.”

Ultimately, Fair Housing Act compliance in rental advertising isn’t just about avoiding legal pitfalls—it’s about fostering inclusivity and equity. By rethinking credit score requirements and adopting a nuanced screening approach, landlords can attract a diverse tenant base while minimizing the risk of discrimination claims. The key lies in balancing business interests with a commitment to fairness, ensuring that housing opportunities are accessible to all, regardless of their background.

Effective Strategies to Promote Your Club from the Beginning

You may want to see also

Explore related products

![]()

Impact on Tenant Screening

Posting a minimum credit score in a rental advertisement significantly narrows the tenant pool, often excluding individuals with limited credit history or past financial setbacks. This practice disproportionately affects younger renters, immigrants, and those recovering from bankruptcy or medical debt, who may otherwise be reliable tenants. By fixating on a single metric, landlords risk overlooking candidates with stable income, positive rental histories, or strong references. This approach undermines holistic tenant screening, which should consider multiple factors like employment verification, rental references, and debt-to-income ratios.

For landlords, setting a minimum credit score might seem like a shortcut to assessing financial responsibility, but it’s a blunt tool. A tenant with a 700 credit score but erratic income could pose a higher risk than someone with a 650 score and consistent earnings. Screening tools that rely solely on credit scores fail to account for context—such as temporary unemployment or unexpected expenses—that may have impacted a tenant’s credit. Instead, landlords should use credit scores as one of several criteria, paired with other indicators of reliability, to make informed decisions.

From a legal standpoint, posting a minimum credit score requirement can invite scrutiny under fair housing laws. If the policy disproportionately impacts protected classes—such as racial minorities, who statistically have lower average credit scores—it could be deemed discriminatory. Landlords must ensure their screening practices are consistently applied and justified by business necessity. For example, a blanket 700 credit score requirement might be harder to defend than a flexible approach that considers individual circumstances.

To balance risk mitigation and inclusivity, landlords can adopt tiered screening processes. Start with a reasonable credit score threshold, but allow exceptions for tenants who provide additional proof of financial stability, such as larger security deposits or cosigners. Alternatively, use credit reports to identify red flags like frequent late payments or high debt utilization, rather than focusing solely on the score. This approach ensures fairness while still protecting the landlord’s interests.

Ultimately, the impact of posting a minimum credit score in rental advertisements extends beyond tenant exclusion—it shapes the rental market’s accessibility and equity. Landlords who prioritize flexibility and context in screening can attract a broader range of qualified tenants, reduce vacancy rates, and foster positive landlord-tenant relationships. By moving away from rigid credit score requirements, they contribute to a more inclusive housing ecosystem that values potential over past financial missteps.

Free Business Advertising: Top Platforms to Promote Your Brand

You may want to see also

Explore related products

![]()

Alternatives to Credit Score Minimums

Posting a minimum credit score in rental advertisements is a practice that, while common, raises legal and ethical concerns. However, landlords and property managers still need reliable ways to assess a tenant’s financial responsibility. Alternatives to credit score minimums exist, offering more inclusive and nuanced methods to evaluate prospective tenants. These approaches not only mitigate legal risks but also broaden the pool of qualified applicants.

One effective alternative is income verification, which focuses on a tenant’s ability to pay rent rather than their credit history. Landlords can require proof of income, such as pay stubs or bank statements, to ensure the tenant earns at least 2.5 to 3 times the monthly rent. For example, if the rent is $1,500, a tenant should demonstrate a monthly income of $4,500 to $5,000. This method is straightforward and directly tied to rental affordability, reducing the reliance on credit scores.

Another strategy is rental history checks, which assess a tenant’s past behavior in paying rent and adhering to lease terms. Landlords can contact previous landlords for references or use tenant screening services that provide detailed rental histories. A tenant with a consistent record of on-time payments and lease compliance can be a strong candidate, even with a lower credit score. This approach emphasizes proven reliability over numerical metrics.

For tenants with limited credit history, co-signers or guarantors can serve as a viable alternative. A co-signer agrees to take financial responsibility if the tenant fails to pay rent. This reduces risk for the landlord while providing an opportunity for tenants who might otherwise be disqualified due to credit score minimums. It’s important to clearly outline the co-signer’s obligations in the lease agreement to avoid misunderstandings.

Lastly, larger security deposits or prepaid rent can offer landlords additional financial protection without relying on credit scores. For instance, a tenant with a lower credit score might be asked to pay a security deposit equivalent to two months’ rent instead of one. Alternatively, some landlords may accept prepaid rent for several months upfront. These options provide a buffer for landlords while allowing tenants to secure housing without meeting strict credit requirements.

By adopting these alternatives, landlords can create a fairer and more flexible screening process. These methods not only address the limitations of credit score minimums but also align with legal guidelines, such as the Fair Housing Act, which prohibits discriminatory practices. Ultimately, focusing on a tenant’s ability and willingness to pay rent fosters a more inclusive rental market.

Advertising Slot Machine Cafes: Legal, Ethical, and Practical Considerations

You may want to see also

Explore related products

![]()

State-Specific Rental Laws Overview

Rental laws vary significantly across states, and understanding these nuances is crucial for landlords and tenants alike, especially when it comes to advertising minimum credit score requirements. For instance, California prohibits landlords from using credit scores as the sole criterion for tenant screening, emphasizing a more holistic approach that includes income verification and rental history. This contrasts sharply with states like Texas, where landlords have broader discretion in setting credit score thresholds, often explicitly stating minimum requirements in rental ads. Such disparities highlight the importance of local research before crafting or responding to rental advertisements.

In New York, landlords must provide written disclosure if a credit check is part of the application process, and they cannot charge excessive fees for it. This transparency is designed to protect tenants from unfair practices. Conversely, in Florida, while landlords can require a minimum credit score, they must also comply with federal Fair Housing Act guidelines, ensuring that such criteria do not disproportionately impact protected classes. These state-specific rules underscore the need for landlords to balance screening rigor with legal compliance.

For tenants, knowing state laws can empower them to challenge discriminatory practices. In Washington State, for example, landlords cannot reject applicants solely based on credit scores if they can demonstrate alternative financial stability, such as a co-signer or higher security deposit. This flexibility is not universal; in Arizona, landlords often enforce strict credit score minimums without such exceptions. Tenants should therefore familiarize themselves with local tenant rights organizations to navigate these variations effectively.

Landlords must also be cautious about how they advertise credit score requirements. In Illinois, while minimum credit scores can be listed, they must be accompanied by clear explanations of how the score will be used in the screening process. Missteps here can lead to legal challenges under state or federal law. A practical tip for landlords is to consult with a real estate attorney to ensure their advertisements align with both state and federal regulations.

Ultimately, the patchwork of state-specific rental laws demands vigilance from both landlords and tenants. While some states offer flexibility in credit score requirements, others impose strict limitations. Staying informed not only ensures compliance but also fosters fairer rental markets. Whether you’re advertising a property or searching for one, understanding these laws is a non-negotiable step in the process.

Effective TV Advertising Strategies for Vuse: Creative Tips and Compliance

You may want to see also

Frequently asked questions

Yes, in most jurisdictions, landlords can legally include a minimum credit score requirement in rental advertisements, as long as it is applied consistently and does not discriminate based on protected classes.

Posting a minimum credit score requirement generally does not violate fair housing laws unless it disproportionately impacts a protected class (e.g., race, religion, gender) and cannot be justified as a legitimate business necessity.

Some states and localities have specific laws or regulations that may restrict or prohibit the use of credit scores in rental screenings, so it’s important to check local laws before including such requirements in advertisements.

Yes, a landlord can still refuse to rent based on other financial red flags, such as a history of evictions or unpaid debts, even if the applicant meets the minimum credit score requirement.

While not legally required in most cases, offering alternative screening methods (e.g., co-signers, larger security deposits) can help landlords remain flexible and attract a broader pool of qualified tenants.